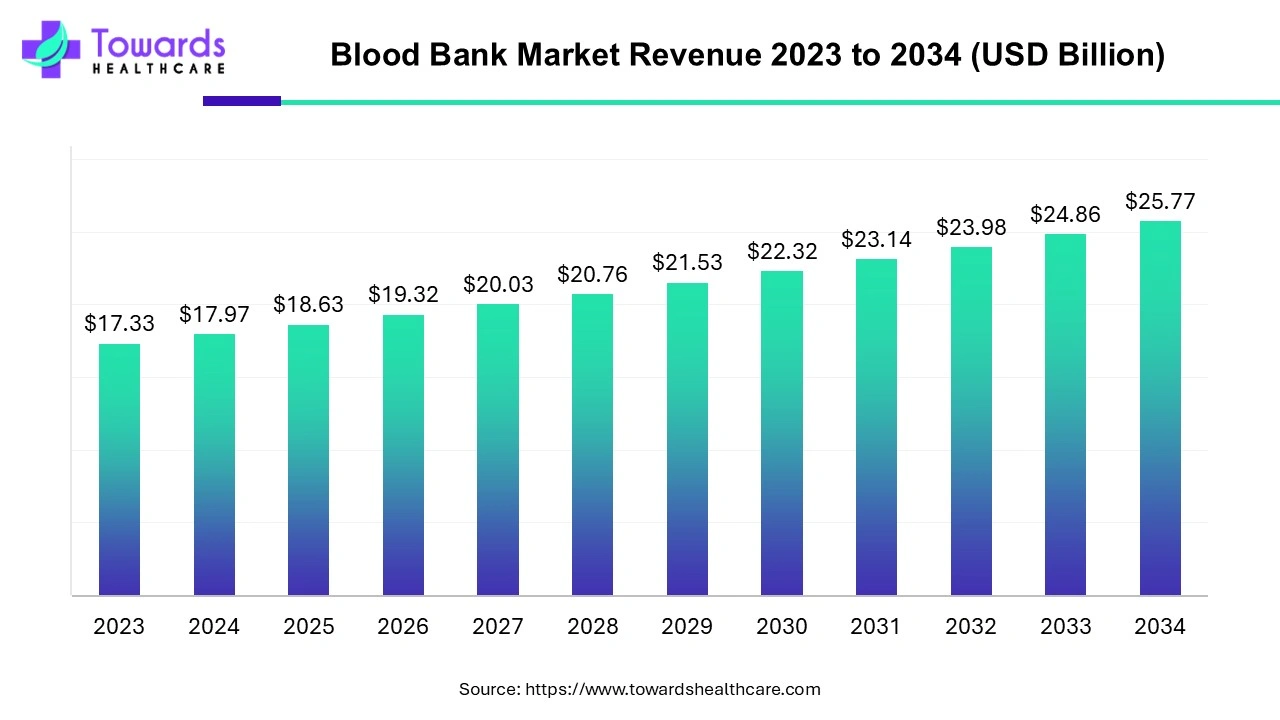

The blood bank (blood banking) market was estimated at US$ 17.33 billion in 2023 and is projected to grow to US$ 25.77 billion by 2034, rising at a compound annual growth rate (CAGR) of 3.7% from 2024 to 2034.

A blood bank is a center where donated blood is collected, stored, and preserved for later use in blood transfusion. Blood banking is the process of blood collection, processing, testing, separation, and storage. It includes typing the blood for transfusion and testing for infectious diseases such as hepatitis B, hepatitis C, HIV, and West Nile Virus. Blood banks also store blood components like red blood cells (RBCs), white blood cells (WBCs), platelets, and plasma.

The increasing incidences of hematological disorders and rising blood donation awareness promote the market. Hematological disorders such as anemia, blood cancer, hemophilia, thalassemia, sickle cell disease, thrombocytopenia, etc. require blood transfusion. Apart from these disorders, blood transfusion is required for supportive care in cardiovascular surgery, transplant surgery, and massive trauma. According to the WHO, around 118.5 million blood donations are collected globally every year. Additionally, recent technological advancements simplify blood collection, storage, and processing, potentiating market growth.

The increasing demand for blood and blood components due to increased population, hematological disorders, and the number of surgeries necessitates novel advancements in efficient blood collection, storage, and transportation. Advanced technologies like artificial intelligence (AI), machine learning (ML), blockchain technology, RFID, and IoT govern high levels of accuracy, traceability, automation, and reliability in the blood transfusion process, resulting in reduced errors. RFID tags aid in the constant monitoring of the blood bags to ensure their quality. It can also reduce the misidentification of patients and blood products during transfusion. IoT can track real-time data about donors and receivers and transport of blood products, improve inventory management, and trace the entire procedure. Additionally, these advanced technologies can monitor the temperature of the products and enhance the efficiency of the blood supply chain.

The major challenge faced by every blood bank is the short shelf life of blood and blood components. The shelf life of an average blood is 42 days. Hence, blood must be used within this time. Also, blood cannot be frozen for long-term preservation in most cases. Blood banks face logistical difficulties since they need to maintain consistent, cool, but not frozen storage. Another challenge is the resistance of patients to new blood, increasing the chances of graft-versus-host disease (GVHD).

")

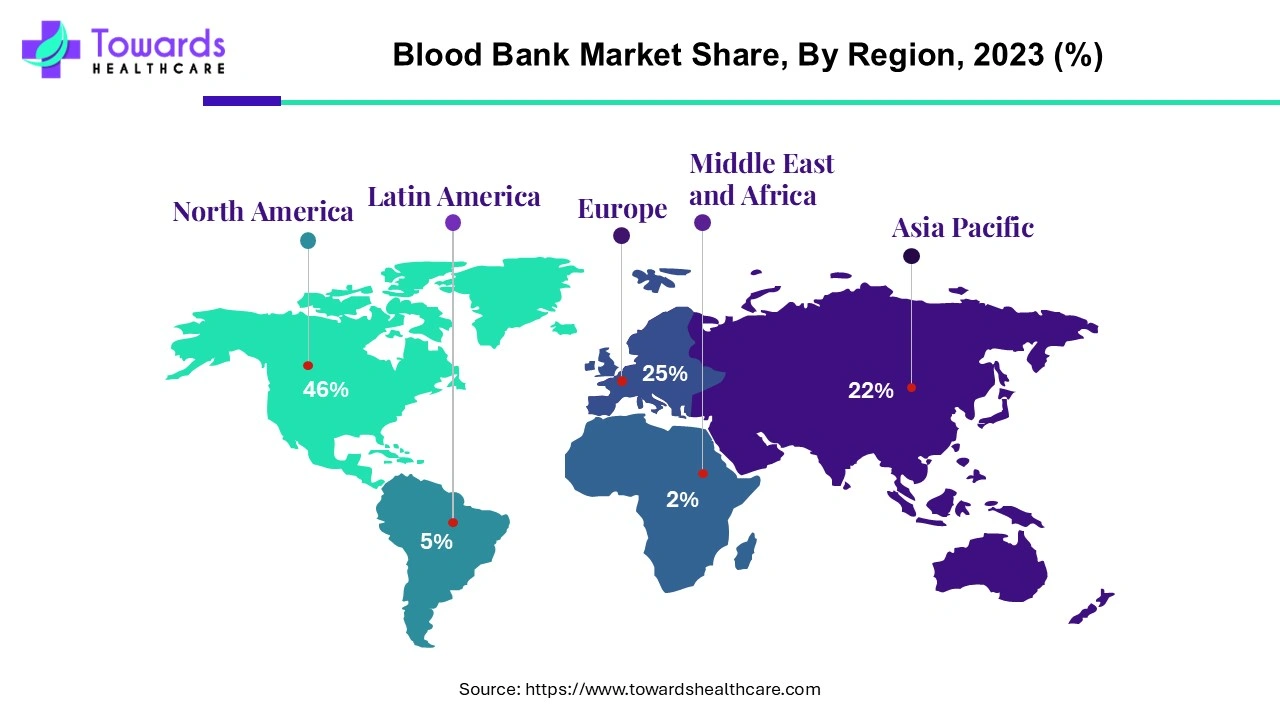

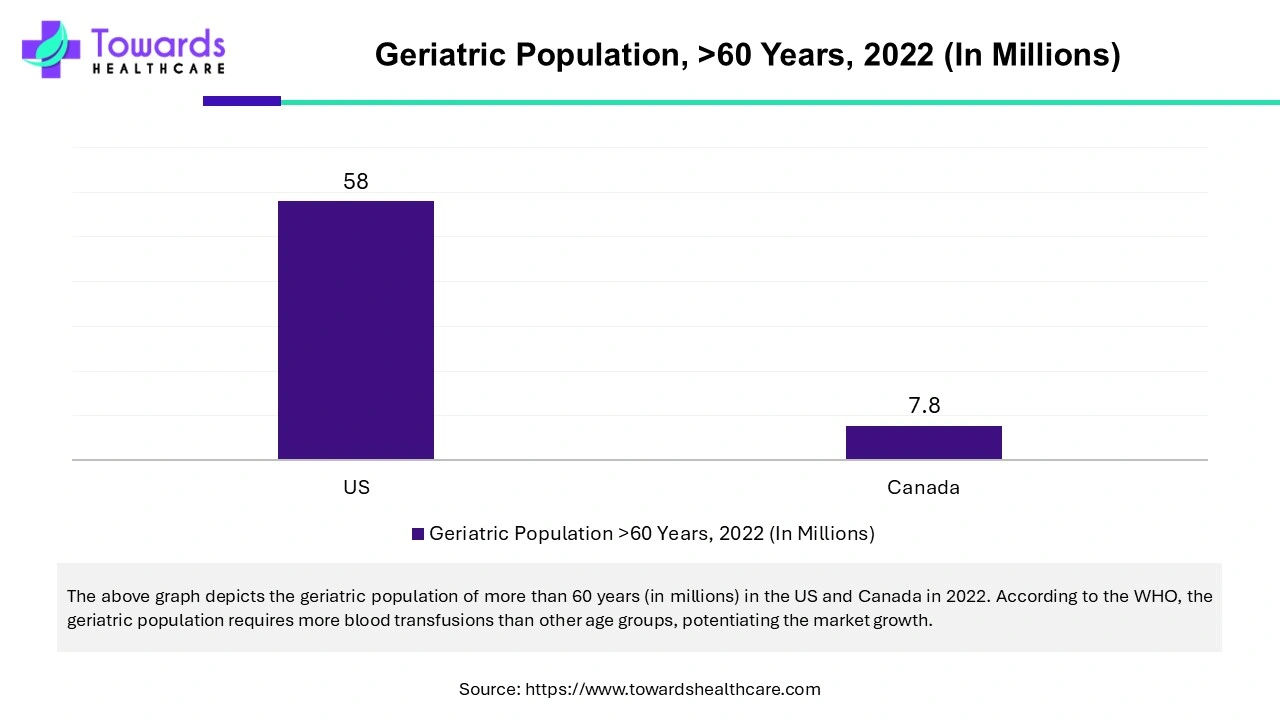

North America dominated the blood bank (blood banking) market by 46% in 2023. The increasing geriatric population, the number of surgical operations, increasing awareness of blood donations, and increasing investments drive the market. According to the Association of Blood Donor Professionals, around 3% of the eligible US population donates blood annually. There are about 90 U.S. FDA-registered hospital-based blood centers and 53 community blood centers in the U.S. The blood banks in the US are regulated by the Food and Drug Administration and the American Association of Blood Banks. Additionally, established healthcare infrastructure and regional government blood donation efforts promote market growth.

")

Asia-Pacific is anticipated to grow fastest in the blood bank (blood banking) market during the forecast period. The rising geriatric population, increasing incidences of hematological disorders, and favorable government policies drive the market. According to The Lancet report, there are more than 400 blood centers in China, while India has 3840 licensed blood banks. India collects over 1.61 million blood units annually. In Japan, there were 9.9 million blood donations between 2020 and 2021. This increase in awareness of blood donations augments the market. Countries like China, India, and Japan hold several blood donation camps to increase awareness and promote blood donations in the respective nations. Such camps are also held to fulfill the blood and blood components demands of the patients.

Europe is expected to grow significantly in the blood bank market during the forecast period. The hospital and the industries in Europe are increasing the demand for blood banks, which is promoting the market growth. Due to increasing research and development, the demand for well-developed blood banks is increasing in the UK. Furthermore, it is also supported by the government investments. The hospitals in Germany are increasing the demand for blood banks due to the increasing treatments that require urgent need of blood.

By product, the red blood cells segment registered its dominance over the global blood bank (blood banking) market in 2023 and is expected to grow fastest during the forecast period. The RBC component experiences the highest demand among all fresh components due to rising incidences of anemia and the number of surgeries. According to The Lancet report, around one-fourth of the global population is estimated to be anemic, with 1.92 billion people with anemia in 2021. The risk is high among women, expectant mothers, young girls, and children less than 5 years. Around 310 million major surgeries are performed annually worldwide, enhancing the demand for RBCs.

By function, the testing segment held a dominant presence in the blood bank (blood banking) market in 2023 and is projected to expand rapidly over the coming years. The first and foremost step of a blood bank is the testing of collected blood. The blood that is collected from the donor is tested for the type of blood group and Rh typing. It is also screened for unexpected RBC antibodies and infectious diseases. Various tests for syphilis, HIV, hepatitis, and malaria are performed to prevent rejection in the receiver. The incidences of graft-versus-host-disease (GVHD) promote the segment growth.

By end user, the hospital segment held the largest share of the blood bank (blood banking) market in 2023 and is anticipated to grow with the highest CAGR in the market during the studied years. The increasing number of surgeries and accidents, more number of patients, and favorable infrastructure boost the segment growth. The demand for blood and blood components is higher in hospitals due to the high number of emergency cases of patients.

By Product

By Function

By End User

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar