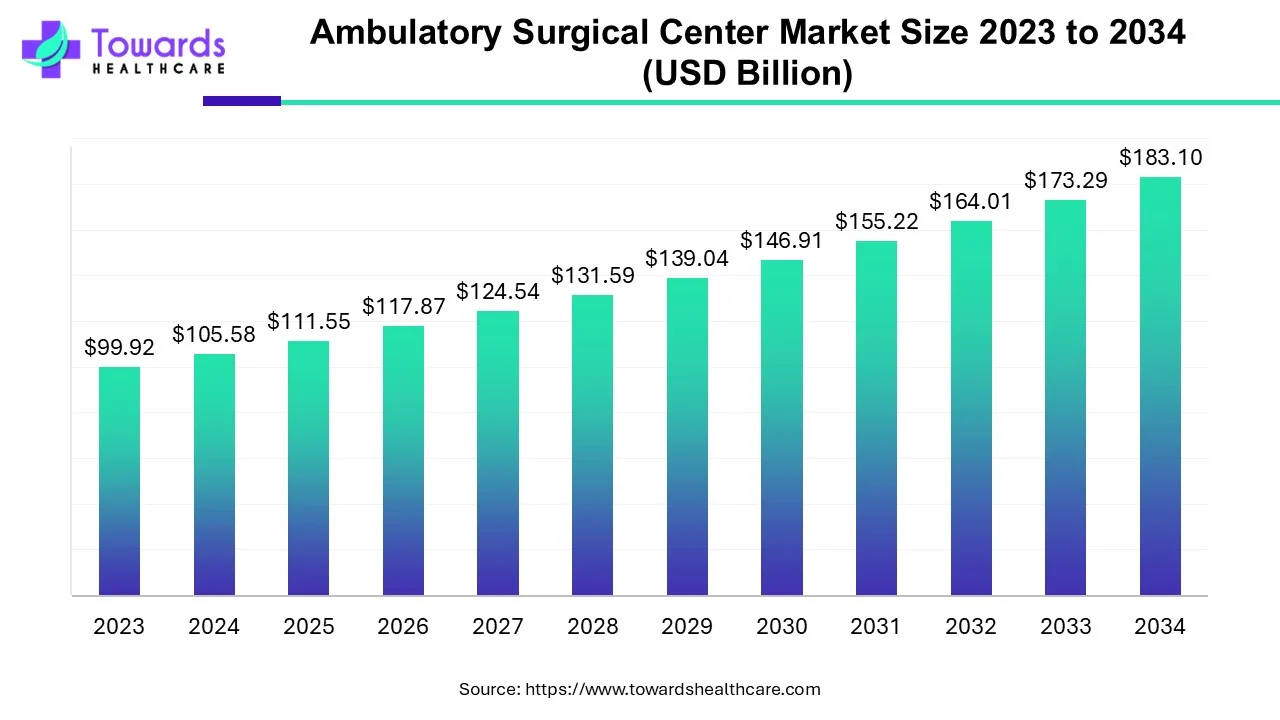

The ambulatory surgical centers market accounted for USD 105.58 billion in 2024 and is predicted to increase to USD 183.1 billion by 2034 and is poised to grow at a CAGR of 5.66% from 2025 to 2034. The increasing number of surgeries, growing demand for outpatient settings, and technological advancements drive the market.

Ambulatory surgery centers (ASCs) are specialized medical facilities that offer outpatient surgical services. Outpatient refers to a patient who is not admitted to a hospital and can leave on the same day of their surgery. Before the advent of ambulatory surgery centers in the 1970s, nearly all surgical procedures were conducted in hospital settings. While hospitals can be relied on to provide quality treatment, patients seeking elective surgery face several challenges, including scheduling delays and restricted operating room availability. ASCs have been a popular alternative to inpatient hospital settings in recent decades due to their flexible scheduling options, calmer and more comfortable environments, and cheaper prices.

Ambulatory Surgery Centers (ASCs) offer significant value through high-quality outcomes and lower-cost care, making them the optimal choice for many healthcare procedures for the right patients at the right price. Currently, over 80% of surgeries are conducted in an outpatient setting, largely due to the innovations driven by ASCs that have revolutionized outpatient surgery. These advancements in technology and techniques have enhanced the safety and comfort of outpatient procedures. With the aging population in America, particularly the baby boomers, the demand for the services provided by surgery centers is on the rise.

Presently, more than 49 million people, or 15% of the U.S. population, are 65 or older, and this demographic is projected to grow to 24% by 2060. ASCs also contribute to reducing healthcare expenses for patients, insurers, and Medicare, achieving a one-year savings of $42.2 billion in healthcare spending and creating $4.2 billion in annual Medicare savings by offering an alternative to traditional hospital settings.

The integration of Artificial Intelligence (AI) is set to significantly enhance growth in the Ambulatory Surgical Center (ASC) market. AI technologies, such as machine learning and data analytics, streamline various aspects of surgical operations and patient care. One of the primary benefits is improved diagnostic accuracy; AI algorithms can analyze medical imaging with exceptional precision, aiding in quicker and more accurate diagnoses. Additionally, AI-driven predictive analytics assist in anticipating patient needs and optimizing surgical schedules, which enhances operational efficiency and reduces waiting times.

AI also enhances patient outcomes through personalized treatment plans. By analyzing vast datasets, AI can tailor interventions to individual patient profiles, potentially leading to better results and fewer complications. Furthermore, robotic-assisted surgeries, powered by AI, offer high precision and minimally invasive options, which contribute to faster recovery times and reduced hospital stays.

Overall, AI integration in ASCs is driving innovation, improving efficiency, and enhancing patient care. This technological advancement is expected to spur market growth by attracting investments and meeting the increasing demand for advanced, high-quality surgical services.

The shift from surgical procedures in hospitals to ambulatory settings is the factor influencing the growth of the ACS industry. Over the last decade, the number of surgical procedures performed in ambulatory surgery facilities has increased significantly. Given the factors like as shorter stays, innovative technologies, cost-effective surgical procedures, and lower infection risks, a large number of patients select these healthcare facilities for various surgeries.

Outpatient surgical volume in ambulatory surgical facilities, for instance, has increased over the last decade, according to data from the Medicare Payment Advisory Commission and VMG Health. ASCs performed nearly 60% of outpatient procedures in 2019, compared to 48% in 2010. Ambulatory surgery centers (ASCs) are redefining healthcare delivery as well as the medical device and equipment industry. ASCs can offer surgical treatments at rates 35% to 50% lower than hospitals by focusing on standard, lower-risk procedures in a more convenient location. This benefits the US healthcare system an estimated $40 billion per year while also influencing ASC growth. In 2018, 5,700 ASCs in the United States completed 23 million procedures and earned $35 billion in revenue.

Broad industry trends are driving the growth of ASCs, the first of which was established in 1970. A consistent increase in healthcare spending has put a strain on costs and margins across the industry, promoting a shift to outpatient treatment. Payers are assisting in the shift of procedures to ASCs by lowering provider reimbursements for hospitals and lowering patient copayments for outpatient procedures.

Increasing government investments toward developing new ambulatory settings are expected to drive industry growth. Moreover, Due to weakened immunity and aging, the elderly population is more vulnerable to infectious and chronic diseases. Chronic diseases are a leading cause of disability and mortality in both developing and developed countries. This indicates a critical need for technologically advanced ambulatory surgical centers capable of providing superior patient care.

The increasing number of surgeries due to several reasons, such as the increasing prevalence of chronic disorders, incidences of acute disorders, and road accidents drive the market. It is estimated that more than 300 million surgical procedures are performed annually worldwide to minimize disability and avoid preventable deaths due to surgically treatable conditions. The most common surgery in the world is a cesarean section (C-section), followed by cataracts, hernia, and aesthetic surgeries. ASCs are highly regulated healthcare facilities that meet extensive state and federal requirements to ensure safety and quality. More than 80% of surgeries are performed in outpatient settings in the US. Favorable government policies and technological advancements favor the development of ASCs.

The high costs associated with advanced medical devices are a major factor hindering the growth of the ambulatory surgical center industry. The equipment required for complex surgical procedures is complex and expensive, with high costs for procurement, installation, and maintenance. Smaller healthcare facilities struggle to meet the growing demand for sophisticated technologies in neurosurgery, cardiovascular surgery, interventional cardiology, and orthopedic surgery. In the United States, a cutting-edge portable digital X-ray unit costs more than US$ 100,000 on average. Even basic medical equipment, such as an operating table, can cost more than US$ 50,000.

Over the last decade, a sizable portion of the patient population in the United States has indicated a preference for having surgical procedures performed at outpatient surgery centers. However, the market's expansion is expected to be hampered over the aforementioned term by several drawbacks associated with ASCs. Among these disadvantages are the lack of overnight accommodations, the possibility of difficulties and crises during some surgical procedures, and the lack of any contingency plans. If complications or issues arise during a surgical procedure, patients may be transferred from ambulatory surgical centers to hospitals in the surrounding area.

As a result, some patients prefer to have their surgical procedures done in hospitals. According to a research report distributed by the National Center for Biotechnology Information (NCBI) in 2017, the rate of complications and adverse events as a result of orthopedic procedures performed at ASCs was between 0.05 percent and 20.0 percent. The most common complications during surgical procedures include pain and nausea, poor recovery, and infection. The industry's growth may be hampered by these disadvantages.

One of the key drivers of industry growth is reimbursement. Favorable reimbursement policies are driving the Centers for Medicare & Medicaid Services (CMS) to expand the list of surgical procedures that are permitted in ASCs. Rising commercial payer initiatives to encourage physicians to perform various surgical procedures in these facilities are expected to fuel the industry in future payers. Furthermore, CMS is constantly reviewing the complications associated with surgical procedures, thereby improving patient safety when undergoing surgical procedures.

For instance, according to Advisory Board CMS planned to review 38 procedures such as spine surgery, and lumbar, and cervical spinal fusions to determine if they are safely performed in ambulatory settings in September 2018. Payers' intense focus on the safety of surgical procedures in these healthcare facilities will attract a larger patient pool throughout the United States. Thus, the favorable reimbursement scenario for procedures performed in ambulatory settings, combined with a greater emphasis on procedure safety, is expected to propel industry growth in the future.

The ambulatory surgical center is segmented based on the type of center, ownership, and application. Based on the type of center, the industry is further segmented into single-specialty and multispecialty. The single-specialty segment dominates the industry in 2022 and is anticipated to continue to show similar trends in the coming years. The growing incidence and prevalence of ophthalmic disorders, as well as the strong presence of single-specialty ambulatory surgical centers, account for the dominance of single-specialty settings. During the forecast period, the multi-specialty segment is expected to grow at a significant CAGR. The increasing number of surgical procedures in ophthalmology, gastroenterology, and pain management is expected to boost multi-specialty setting revenue in the coming years.

")

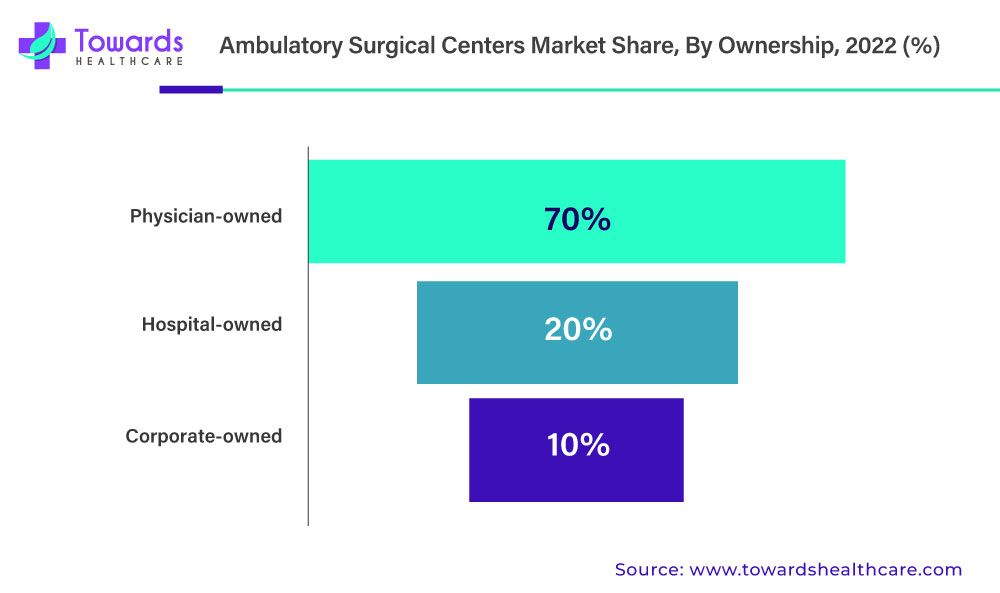

Based on ownership, the ACS industry is further segmented into physician-owned, hospital-owned, and corporate-owned. The physician-owned segment accounted for the largest share in 2022 and is expected to expand at a substantial CAGR during the forecast time. Physician-owned ambulatory settings are the most common, with doctors owning 100% of the stock. The segment's large share is also attributed to factors such as physicians' convenience in scheduling surgical procedures, which has led to an increased preference for this type of ownership in the United States.

In 2022, the hospital-owned segment has the second-highest market share and is expected to grow at a significant CAGR during the forecast period. Increased employment of physician-owned practices by hospital-owned practices is expected to boost hospital-owned center revenue in the future. In the corporate-owned segment, I anticipated expanding at the highest CAGR during the forecast period. This segment's rapid growth can be attributed to the increasing focus of management companies and physicians on the formation of a common joint venture. As partnerships between corporate firms and physicians continue to emerge, the ownership model is expected to boost the revenue of corporate-owned centers in the coming years.

")

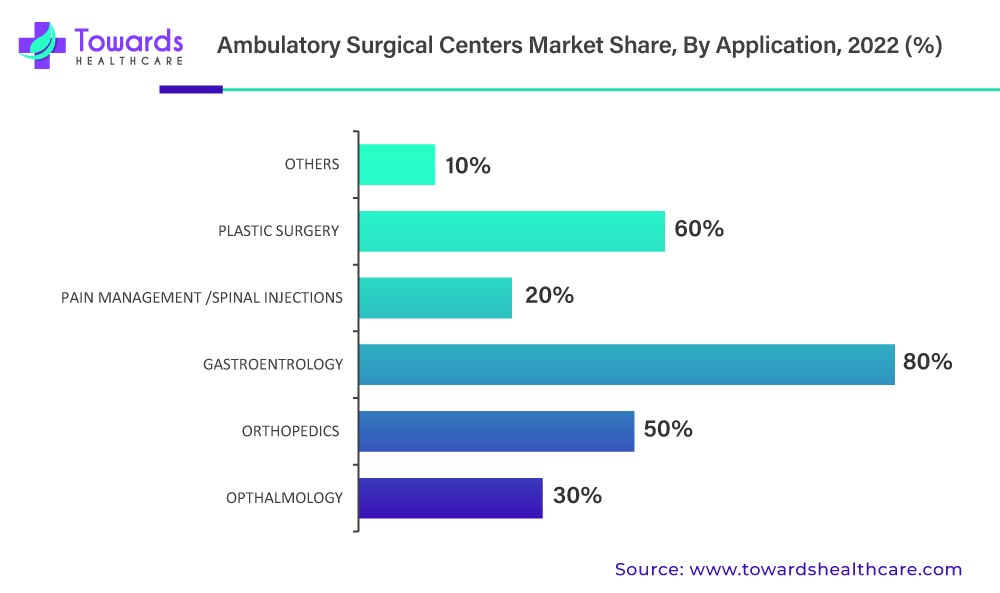

Based on application, the industry is further segmented into ophthalmology, orthopedics, gastroenterology, pain management/spinal injections, plastic surgery, and others. In 2022, the gastroenterology segment dominated the ambulatory surgical center industry, accounting for 35% of total revenue. Given its global reach, the gastroenterology segment accounted for the largest share of the global ambulatory surgical center industry. Plastic surgery, on the other hand, is expected to grow at the fastest rate in the coming years. Patients' preferences for nonsurgical and minimally invasive surgeries are expected to rise, assisting the plastic surgery segment to expand rapidly.

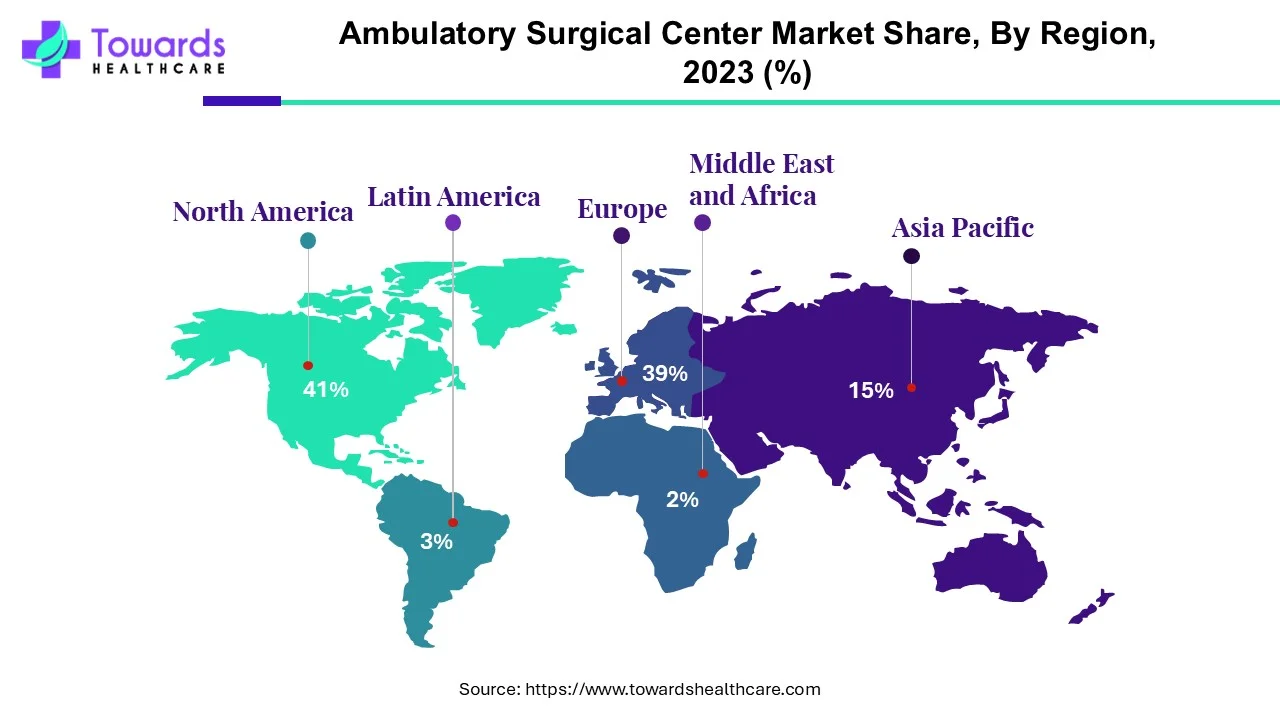

North America dominated the ambulatory surgical center market in 2023. Increased government support for primary care services and expanded outpatient coverage are major factors driving the growth of the ambulatory surgical center market in North America. There are currently 11,255 ASCs in the US, out of which 6,223 ASCs are Medicare-certified. The increasing geriatric population increases the demand for ASC services. Around 15% of the total US population is 65 years and above and it is estimated to grow to 24% by 2060. It is reported that ASCs save Medicare $4.2 billion annually.

The U.S. ambulatory surgery center market is experiencing substantial growth. This is because of the shift towards outpatient care, fostered by convenience, cost-effectiveness, and enhanced patient outcomes. The robotic-assisted surgery programs in ambulatory surgery centers, such as at Southeastern Spine Institute, and strategic investments like Tarrant Capital IP, LLC, invested in Compass Surgical Partners, contributing to the market expansion.

")

Asia-Pacific is anticipated to grow at the fastest rate in the market during the forecast period. The rising prevalence of chronic disorders, increasing healthcare expenditure, and the burgeoning healthcare sector drive the market. Favorable government policies to expand ASCs also support market growth. The growing medical tourism industry in Asia-Pacific also contributes to market growth. The implementation of day surgery in eye hospitals in China accounts for more than 70% of elective surgery. The increasing investments and collaborations among key players promote the development of ASCs. Countries like China, Japan, and South Korea are at the forefront of developing ASCs.

The Indian ambulatory surgical center market is experiencing significant growth, owing to increasing healthcare costs, growing demand for outpatient care, and advancements in minimally invasive surgical techniques. Thus, in developing countries like India, it necessitates demand for cost-effective healthcare solutions with a noticeable shift towards outpatient care and ambulatory surgical centers becoming a preferred choice for patients looking for quick recovery at lower costs.

Europe plays a significant role in the ambulatory surgical center market, stemming from increasing outpatient procedures, together with government support for healthcare improvements. Additionally, advancements in minimally invasive surgery, specifically in robotic-assisted surgery, allow more complex procedures to be performed in ambulatory surgical centers, improving precision and control. Various technologically advanced platforms, such as Doctolib in France, are facilitating patients to schedule appointments and access healthcare services online by fostering overall patient experience and streamlining operations in the ambulatory surgical center market.

The rise of the healthcare sector is fueling demand in the ambulatory surgical center industry, which is exacerbated by an increase in research on service portfolios in mobile operative systems. The healthcare industry's major players are investing in research and development to build mobile surgery centers. Businesses primarily increase revenue through acquisitions, mergers, collaborations, and product portfolio enhancement through extensive research and development. To gain a significant market position and maintain industry rivalry in the ambulatory surgical center industry, the major market players are employing a variety of inorganic and organic growth strategies.

By Type of Center

By Ownership

By Application

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar