March 2026

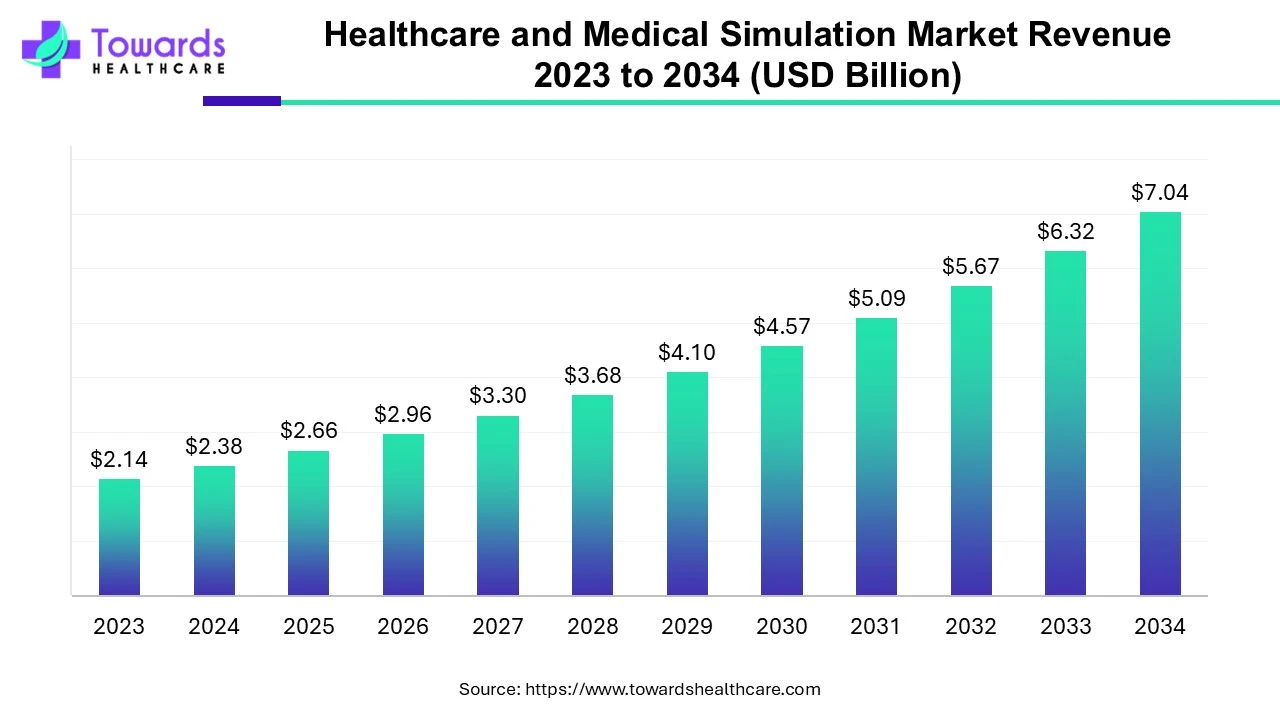

The healthcare and medical simulation market was estimated at US$ 2.14 billion in 2023 and is projected to grow to US$ 7.04 billion by 2034, rising at a compound annual growth rate (CAGR) of 11.44% from 2024 to 2034. Technological advancements, demand for patient safety, and high-quality treatment drive the market.

Healthcare simulation or medical simulation is a modern method to educate and train healthcare professionals to master cognitive, technical, and behavioral skill sets using advanced technologies. The four main purposes of healthcare simulations are education, assessment, research, and health system integration in facilitating patient safety. Healthcare simulation imitates or represents some situation or process so that healthcare workers can gain skills and confidence without the fear of harming a patient or delaying diagnosis and treatment to patients. Simulation centers are built to improve quality and patient safety.

Medical simulation offers numerous advantages such as helping reduce medical errors, building team communication, and improving skills around crisis resource management. The demand for reducing errors and improving patient outcomes drives the need for medical simulation. Students get real-time training and apply theory knowledge without actually involving a patient. This facilitates healthcare professionals in decision-making and reacting to emergencies.

Artificial intelligence (AI) has become a crucial part of healthcare and medical simulation. AI has rapidly emerged due to advancements in algorithms and software. AI-based companies integrate AI and machine learning (ML) in medical simulation to improve their outcome and offer groundbreaking services. AI improves learner’s experiences and aid in clinical skill development before clinical practice. AI can provide education to healthcare professionals in three ways: direct education, supportive education, and learner empowerment. This enables professionals to make timely decisions in emergencies. AI can also lead to improved diagnostic accuracy of professionals, enhanced communication with patients, and better outcomes from rapid response teams.

Enhanced patient care is a priority for many healthcare professionals to achieve high customer satisfaction. The advent of advanced technologies helps healthcare professionals to improve patient care. The demand for enhanced patient care is growing due to increasing awareness, rising demand for better care, keener competition, more healthcare regulation, and the rise in medical malpractice litigation. The quality of patient care is determined by the quality of infrastructure, quality of training, competence of personnel, and efficiency of operational systems. The adoption of healthcare and medical simulation in the healthcare setting helps in the effective training of professionals and primarily focuses on patient care.

The advent of advanced technologies such as artificial intelligence (AI), virtual reality (VR), and augmented reality (AR) revolutionized the entire simulation process. VR enables students to experience visual stimuli delivered via computer graphics and other sensory experiences. AR enables students to interact in real-world environments that are enhanced with virtual imagery. These technologies let students learn how to perform several tasks and procedures involving the human body without ever having to practice on a live patient. Such technologies enhance the overall performance of students and healthcare professionals, providing decision-making ability and better treatment outcomes. AR and VR are helping to train the next-gen healthcare professionals on diagnosis, treatment, rehabilitation, surgery, counseling techniques, etc. Furthermore, AR and VR can give customized training to students and professionals based on their progress and skills. Hence, AR and VR provide numerous opportunities and streamline the healthcare ecosystem.

The major challenge of the market is the high cost of the simulation training, limiting the affordability of the LMIC. This results in improper training for the professionals and students of small healthcare institutions. Another major challenge is the lack of trained professionals to provide appropriate training to the students and staff.

North America held a significant share of the healthcare and medical simulation market in 2023. The presence of key players, technological advancements, and availability of skilled professionals drive the market. The use of medical simulation techniques is governed by the presence of major players in the US. Favorable government policies also boost the market. The Agency for Healthcare Research and Quality (AHRQ) is the lead Federal Agency that significantly invests in research to identify the best ways to use simulation in healthcare. As of 2023, 1114 simulation centers are registered in the US and Canada, out of which 415 centers are accredited.

Asia-Pacific is anticipated to grow fastest in the healthcare and medical simulation market during the forecast period. The rapidly evolving technological advancements, increasing investments & collaborations, and favorable government policies drive the market. The market is also driven by the growing research and development to check the efficacy of simulation systems. Several government agencies support the development of simulation labs and centers in the region. The Japanese government collaborated with the WHO to train and test Pacific Island countries’ readiness to respond to health emergencies through workshops and emergency simulation exercises.

For instance,

By product and services, the anatomical model segment registered its dominance over the global healthcare and medical simulation market in 2023 and is projected to expand rapidly in the market in the coming years. A wide range of anatomical models are used to represent the actual anatomy of the human body. Such models give a precise understanding of the parts of the human body. These models are the primary requirement for healthcare institutions and medical colleges.

By technology, the procedural rehearsal technology segment held a dominant presence in the healthcare and medical simulation market in 2023. Simulation techniques are well-suited for rehearsing elements of a complex procedure or surgery that may be unfamiliar or infrequently performed. This technology is used to significantly improve operative performance and reduce medical errors.

The virtual patient simulation segment is anticipated to grow with the highest CAGR in the market during the studied years. Patient interaction is the biggest fear for medical interns and students. Hence, virtual patient simulation aids patient communication, thereby enhancing clinical reasoning and decision-making skills, boosting confidence, and promoting teamwork.

By end-use, the academic institutes segment led the global healthcare and medical simulation market in 2023. The segmental growth is attributed to the increasing number of medical students in institutes, favorable infrastructure, and growing research on medical simulators.

The hospital segment is expected to grow fastest in the market during the forecast period. Hospitals have sufficient facilities, huge capital investments, and an increasing number of interns for learning advanced medical care.

Jacob Paul, CEO of Nasco Healthcare, commented on his appointment as the new CEO of the company that he is glad to lead the world-class team and to fulfill the company’s mission to prepare healthcare workers to be ready to deliver optimal patient outcomes and save lives using their medical simulation and healthcare training products.

By Product and Services

By Technology

By End-Use

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi ShivarkarMarch 2026

March 2026

March 2026

March 2026

Healthcare and Medical Simulation Market