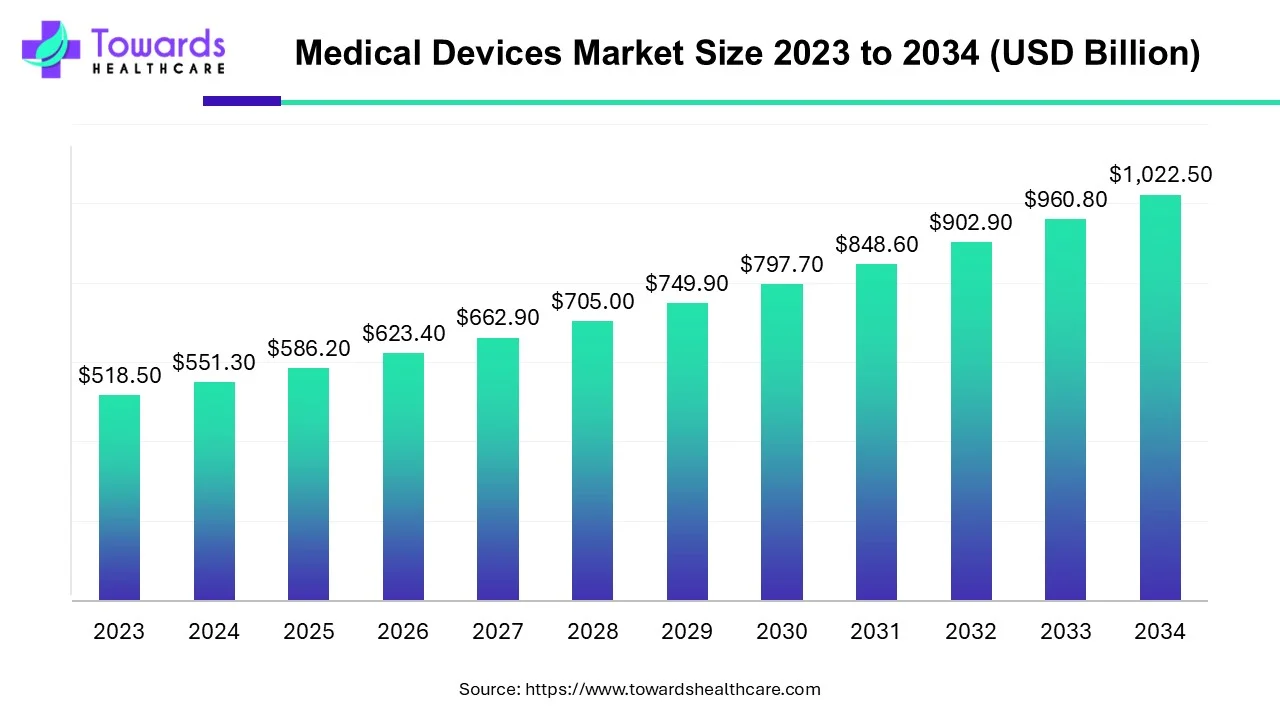

The global medical devices market size is calculated at USD 586.20 billion in 2025, grew to USD 623.37 billion in 2026, and is projected to reach around USD 1083.96 billion by 2035. The market is expanding at a CAGR of 6.34% between 2026 and 2035. Technological advancements and favorable government policies drive the market.

Medical devices are instruments used for various medical purposes, from disease prevention to treatment. The World Health Organization (WHO) defines a medical device as an article, instrument, apparatus, or machine used for detecting, measuring, restoring, correcting, or modifying the structure or function of the body for some health purpose. They range from simple tongue depressors and bedpans to complex programmable pacemakers and closed-loop artificial pancreas systems. It also includes in vitro diagnostics (IVD), such as reagents and test kits. Implants such as cardiac pacemakers are also types of medical devices. There are different types of medical devices based on their use and their purpose.

The rising prevalence and incidences of several acute and chronic disorders potentiate the use of medical devices for different purposes. Technological advancements lead to the latest innovations in medical devices, enhancing efficiency. The increasing investments by both government and private organizations and rising collaborations between industry and academia facilitate the development of medical devices. Favorable government policies and regulatory frameworks support market growth.

")

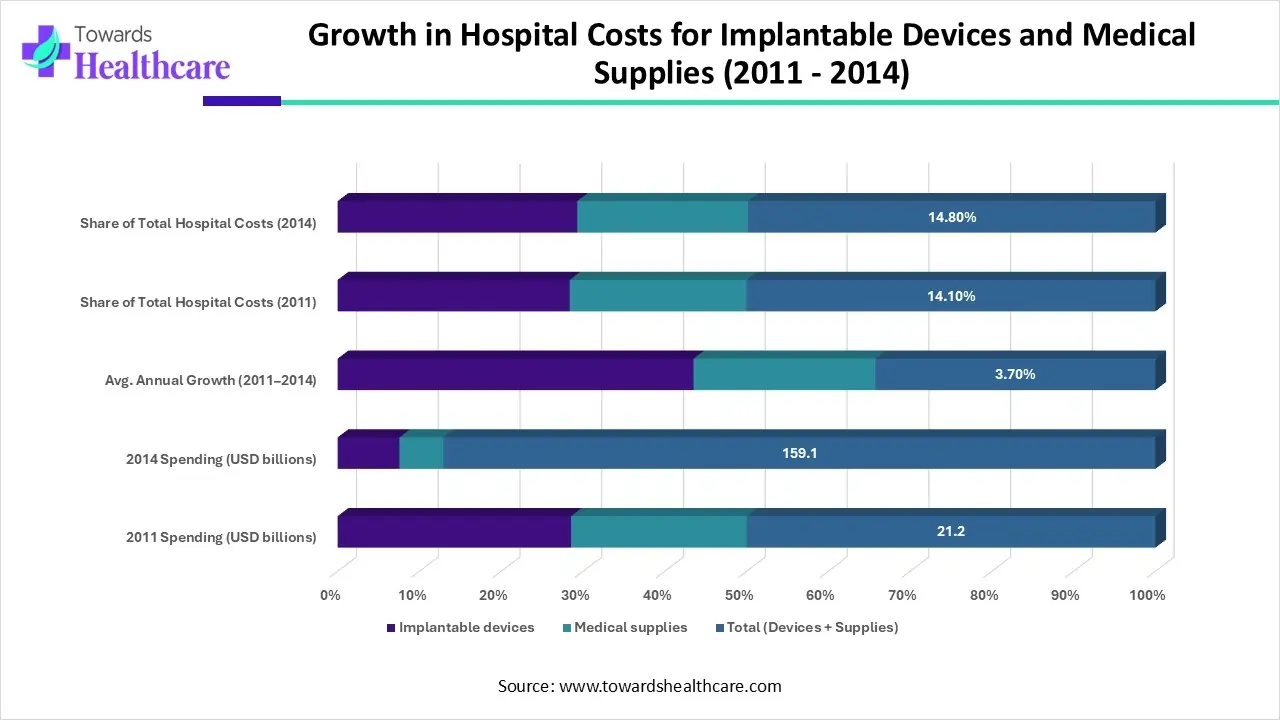

| Category | 2011 Spending (USD billions) | 2014 Spending (USD billions) | Avg. Annual Growth (2011–2014) | Share of Total Hospital Costs (2011) | Share of Total Hospital Costs (2014) |

| Implantable devices | 12.1 | 13.8 | 4.7% | 8.0% | 8.7% |

| Medical supplies | 9.1 | 9.8 | 2.4% | 6.1% | 6.2% |

| Total (Devices + Supplies) | 21.2 | 159.1 | 3.7% | 14.1% | 14.8% |

Between 2011 and 2014, hospitals increased their spending on implantable devices and medical supplies for Medicare-covered services. Spending on implantable devices rose from $12.1 billion to $13.8 billion, growing at an average rate of 4.7% a year. Medical supply expenses also increased, rising from $9.1 billion to $9.8 billion, with a more modest 2.4% annual growth rate.

Together, both categories accounted for 14.1% of total hospital costs in 2011, increasing to 14.8% by 2014, showing that these items consumed a slightly larger share of hospital budgets over time. Total hospital costs overall grew from $150.2 billion to $159.1 billion, reflecting a 2% annual growth rate.

These figures are based on Medicare cost reports from 3,002 hospitals using consistent reporting periods. Actual spending on implantable devices may be even higher, since some hospitals record certain devices like coronary stents under other cost report sections.

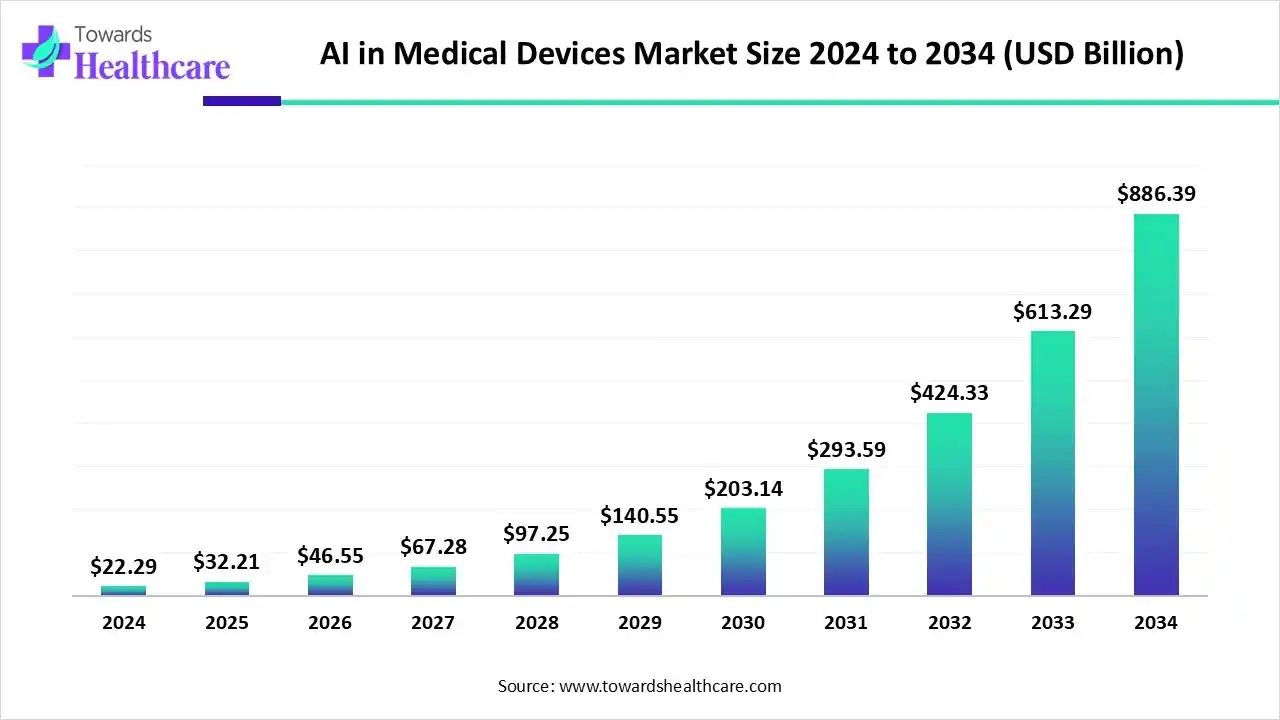

Artificial intelligence (AI) has been found to disrupt the medical device sector by enhancing accuracy and improving overall patient outcomes. Integrating AI into medical devices leads to the development of smart medical devices. These devices provide real-time patient data to healthcare professionals, improving patient outcomes and reducing costs. AI-based tools based on machine learning (ML) algorithms enable online assessment tests for faster treatment and prevent diagnostic errors. AI can also monitor the vital signs of patients and track their physical activity. This helps many healthcare professionals make timely decisions. AI-enabled robotics assist surgeons in performing complex surgical tasks, reducing manual errors. Additionally, AI and ML can automatically adjust medications from implants, such as altering insulin dosages to maintain healthy blood sugar levels.

The global AI in medical devices market was valued at USD 22.29 billion in 2024 and increased to USD 32.21 billion in 2025. It is expected to reach approximately USD 886.39 billion by 2034, growing at a robust CAGR of 44.53% between 2025 and 2034.

")

Driver

Increasing Accessibility

The major growth factor of the medical devices market is the provision of increasing accessibility of medical devices. The rising prevalence of severe chronic disorders such as cancer and COVID-19 necessitates the distribution of medical devices to all regions of the world. Medical devices are primarily required for specific populations, such as the geriatric population, pregnant women, and newborns. The WHO’s Priority Medical Device Project helps improve access to suitable medical devices, increase safety, support quality of care, and strengthen healthcare systems. Apart from the WHO, several government organizations, especially in low- and middle-income countries, take necessary measures to increase access to medical devices. Thus, making medical technology more widely available is essential to make healthcare accessible and more effective.

Restraint

Lack of Regulatory Policies in Certain Nations

The major challenge faced by the market is the lack of appropriate regulatory frameworks in certain developing nations. Many African countries do not have the knowledge and resources to regulate medical devices. They usually rely on European or U.S. regulatory bodies’ approvals and clearances. This impacts the local manufacturers as the compliance cost can be prohibitive, and using devices that are not meant for local needs and issues.

Opportunity

Technological Advancements

The future of the medical devices market is promising, driven by technological advancements leading to the latest innovations. Over the past many decades, significant improvements have been made in the medical device sector. Advancements in telemedicine platforms, wearable devices, robotics, 3D printing, nanotechnology, and augmented & virtual reality. These advancements improve precision, lead to personalization, and enhance the effectiveness of patient care. Integrating these technologies into medical devices enables manufacturers to stay competitive in the market and create more intelligent and connected devices. The increasing investments and growing research and development activities promote the adoption of advanced technologies in medical devices. These advancements also help to cater to the unmet needs of healthcare providers and patients. Thus, advanced technologies create ample future opportunities not only for manufacturers but also for healthcare professionals and patients.

| Table | Scope |

| Market Size in 2025 | USD 586.20 Billion |

| Projected Market Size in 2035 | USD 1083.96 Billion |

| CAGR (2026 - 2035) | 6.34% |

| Leading Region | North America by 40% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Type, By End-User and By Region |

| Top Key Players | Archimedic, Baxter International, Becton, Dickinson & Company, Cardinal Health, Dr Morepan, Fresenius Medical Care, GE Healthcare, Harsoria Healthcare Pvt. Ltd., Johnson & Johnson, Medtronic, Omnia Medical, Siemens Healthineers, SpineGuard, Stryker Corporation, University Medical Devices |

| Segments | Shares % |

| In vitro Diagnostics | 16% |

| Diabetes Care | 11% |

| Dental Devices | 6% |

| Ophthalmic Devices | 7% |

| Nephrology | 5% |

| Orthopedic Devices | 10% |

| Cardiovascular Devices | 13% |

| Diagnostic Imaging | 12% |

| Minimally Invasive Surgery | 8% |

| Wound Management | 4% |

| General Surgery | 5% |

| Others | 3% |

Which Type Segment Dominated the Medical Devices Market?

Medical Devices Market Size, By Type (USD Billion)

| Year | In vitro Diagnostics | Cardiovascular Devices | Diabetes Care | Orthopedic Devices | Dental Devices |

| 2024 | 88.0 | 67.3 | 58.0 | 56.0 | 39.8 |

| 2025 | 92.3 | 71.3 | 61.0 | 59.4 | 42.1 |

| 2026 | 97.0 | 75.6 | 64.2 | 62.9 | 44.4 |

| 2027 | 101.9 | 80.1 | 67.6 | 66.7 | 47.0 |

| 2028 | 107.0 | 84.9 | 71.2 | 70.7 | 49.6 |

| 2029 | 112.5 | 90.0 | 75.0 | 75.0 | 52.5 |

| 2030 | 118.2 | 95.4 | 79.0 | 79.5 | 55.5 |

| 2031 | 124.2 | 101.1 | 83.2 | 84.3 | 58.7 |

| 2032 | 130.6 | 107.2 | 87.6 | 89.4 | 62.0 |

| 2033 | 137.3 | 113.6 | 92.3 | 94.8 | 65.6 |

| 2034 | 144.4 | 120.4 | 97.3 | 100.5 | 69.4 |

By type, the in vitro diagnostics segment held a dominant presence in the market by 16% share in 2025. In vitro diagnostics (IVDs) are devices that can detect a disease, condition, or infection. This segment is dominated because favorable government policies encourage screening and early detection of diseases, favoring the use of in vitro diagnostics. It is estimated that there are currently 40,000 IVDs available. The growing demand for point-of-care diagnostics promotes the segment’s growth. Numerous regulatory agencies are making efforts to increase access to IVDs in many low- and middle-income countries. IVDs are very essential as they affect the majority of clinical decisions.

Diabetes Care Segment: Fastest-Growing

By type, the diabetes care segment is anticipated to grow with the highest CAGR in the market during the studied years. Numerous medical devices are available for diabetes care, such as glucose monitoring devices, insulin pumps, connected continuous glucose monitoring and insulin pumps, and smart insulin pens. The rising prevalence of diabetes and technological advancements boost the segment’s growth. The increasing affordability of blood glucose monitoring devices potentiates their use, eliminating the need to visit a pathology laboratory or other healthcare setting. Many insurance companies cover the cost of diabetes care devices, contributing to the segment’s growth.

| Segments | Shares % |

| Hospitals & ASCs | 68% |

| Clinics | 24% |

| Others | 8% |

Why Did the Hospitals & ASCs Segment Dominate the Medical Devices Market?

By end-user, the hospitals & ASCs segment led the global market by 68% share in 2025. The segmental growth is attributed to favorable infrastructure and suitable capital investment. Suitable capital investments enable hospitals and ASCs to adopt advanced and innovative medical devices for enhanced patient care. The availability of specialized equipment also governs the segment’s growth. Favorable reimbursement policies encourage patients to prefer hospitals & ASCs. Moreover, the presence of skilled professionals assists in operating medical devices.

Clinics Segment: Significantly Growing

By end-user, the clinics segment is predicted to witness significant growth in the market over the forecast period. Clinics utilize a wide range of medical devices, such as diagnostic equipment, surgical instruments, durable medical equipment, and rehabilitation tools. The increasing number of specialized clinics and the availability of advanced medical devices propel the segment’s growth. There are around 72 NCI-Designated Cancer Centers in the U.S. to deliver cutting-edge cancer treatment.

")

North America held the largest share of 40% of the medical devices market in 2025. Advanced healthcare infrastructure and favorable government policies drive the market. Technological advancements and state-of-the-art research and development facilities promote the development of advanced medical devices. The increasing investments and collaborations also contribute to market growth. The growing awareness of innovative medical devices and favorable government and private reimbursement policies support the market. The increasing number of MedTech startups also leads to the development of novel and innovative medical devices in North America.

U.S. Market Trends

Favorable regulatory frameworks and new product launches boost the market. The rising adoption of advanced technologies such as AI promotes the market. The U.S. FDA approved around 1,000 AI-powered medical devices from 1995 to August 2024. Suitable trade policies facilitate market growth. In 2023, the U.S. was the largest exporter of medical instruments, accounting for $34.8 billion. The U.S. exports most of its medical devices to the Netherlands, China, Germany, Mexico, and Japan.

Canada Market Trends

The market is mainly driven by the presence of key players. Around 89 MedTech companies in Canada, including 3M Canada, Abbott, and Alcon Canada, Inc., hold a major share of the market. The rising healthcare expenditure in Canada encourages patients to use advanced medical devices. Canada’s total health spending was around $344 billion in 2023, accounting for 12.1% of its GDP. More than 70% of the healthcare spending is publicly funded through general tax revenues.

Asia-Pacific is projected to host the fastest-growing medical devices market by 24% share in the coming years. The rising prevalence of acute and chronic disorders and the increasing geriatric population boost the market. The growing research and development activities lead to new product launches, propelling the market. The availability of suitable manufacturing infrastructure encourages foreign manufacturers to set up their manufacturing facilities in Asia-Pacific countries. The increasing adoption of advanced technologies enables manufacturers to strengthen their global market presence.

China Market Trends

Favorable government policies and new product launches are the major growth factors that positively impact the market’s growth. The Chinese NMPA announced incentives for foreign manufacturers that open facilities in China by making the application process easier and faster. The increasing government investments to strengthen the medical device sector and the rising healthcare expenditure fuel the market.

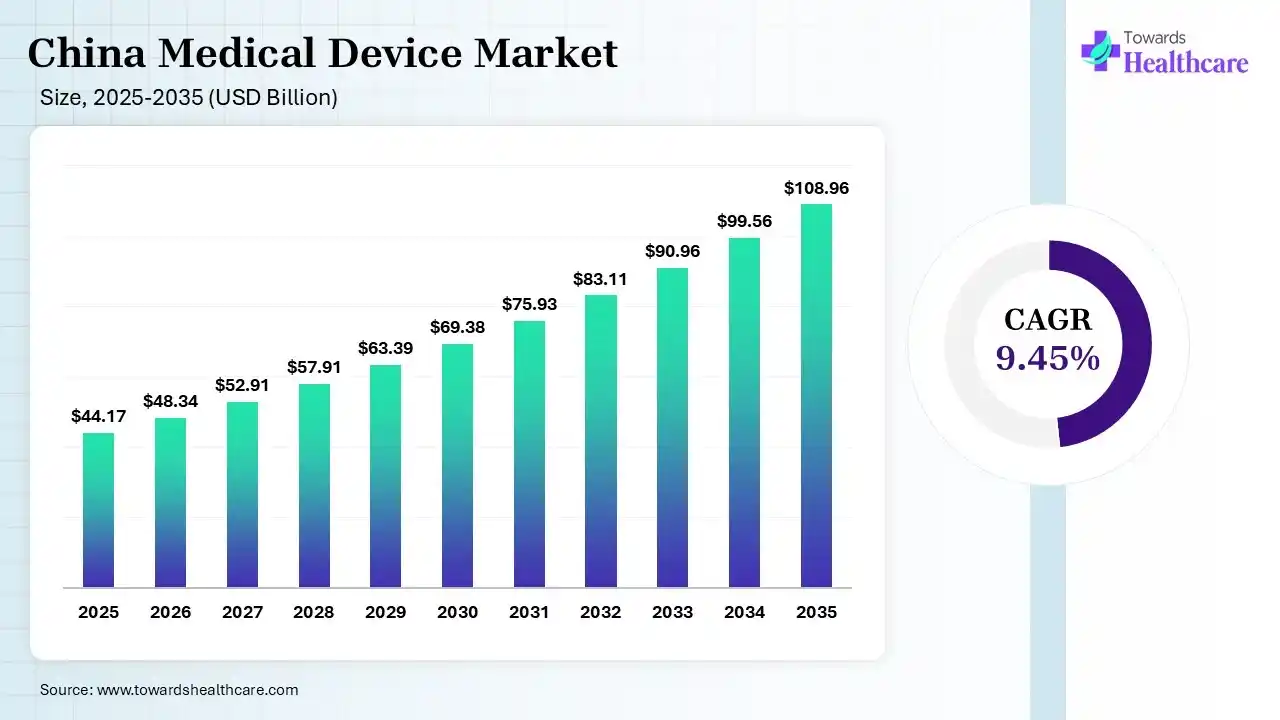

The China medical device market size was estimated at USD 44.17 billion in 2025 and is predicted to increase from USD 48.34 billion in 2026 to approximately USD 108.96 billion by 2035, expanding at a CAGR of 9.45% from 2026 to 2035. The Chinese medical device market is growing because of a rising aging population, increasing chronic diseases such as diabetes and cardiovascular diseases, and a shift toward home medical care.

")

India Market Trends

The Indian Government is making constant efforts to promote the regulation, manufacturing, use, and trade of medical devices in India. It supports the indigenous manufacturing of medical devices through the “Make in India” policy. The Indian Government allows 100% foreign direct investment (FDI) into its medical device sector. The PLI Scheme for Promoting Domestic Manufacturing of Medical Devices with a total financial outlay of Rs 3,420 crore and production tenure from FY 2022-23 to FY 2026-27.

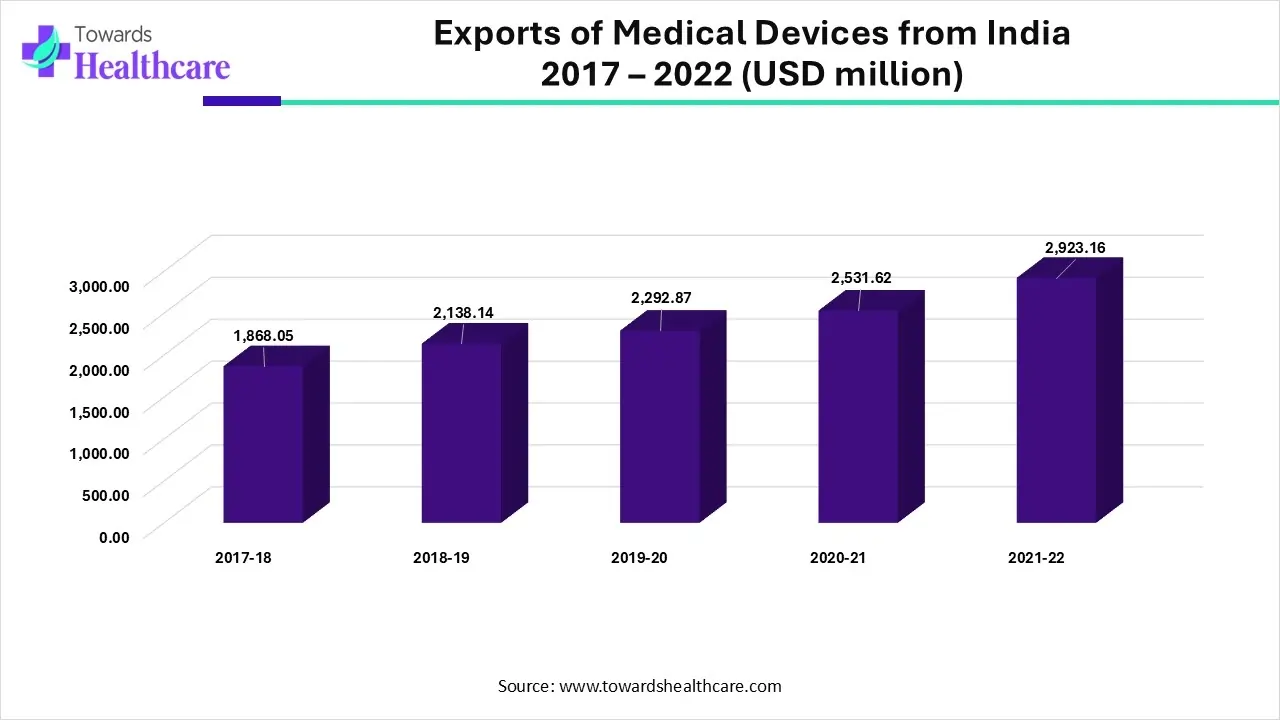

Exports of Medical Devices from India (2017-2022)

| Financial Year | Exports of Medical Devices (USD million) |

|---|---|

| 2017-18 | 1868.05 |

| 2018-19 | 2138.14 |

| 2019-20 | 2292.87 |

| 2020-21 | 2531.62 |

| 2021-22 | 2923.16 |

")

Every year, India increased its medical device exports and strengthened its position in the global market. This steady growth shows that India is producing more high-quality medical devices, improving its manufacturing capabilities, and meeting the rising demand from international markets. The consistent upward trend highlights the industry’s strong performance and India’s growing role as a reliable medical device supplier worldwide.

Japan Market Trends

The Pharmaceuticals and Medical Devices Agency (PMDA) regulates the approval of medical devices in Japan. The increasing geriatric population and the rising number of patients with chronic and lifestyle diseases favor market growth. There are currently 36.25 million people, or one-third of the Japanese population, with 65 years or above. Most of the medical devices in Japan are imported from the U.S., accounting for 60% of the total imports.

Europe is estimated to grow at a considerable growth rate by 28% share in the medical devices market in the upcoming period. The rising adoption of advanced technologies, favorable trade policies, and the presence of key players fuel the market. Key players such as Siemens Healthineers, Medtronic, and Fresenius Medical Care hold a major share of the market. European Union and European Medicines Agency regulate the approval of medical devices in Europe. The growing awareness of enhanced patient care and treatment outcomes promotes the use of innovative medical devices.

Germany Market Trends

Germany is the third-largest medical technology market globally after the U.S. and Japan. The growing research and development and the increasing number of patents facilitate market growth. In 2023, more than 15,000 patent applications were filed with the European Patent Office (EPO) in the field of medical technology. It is estimated that around 500,000 types of medical devices and in vitro diagnostics are available in Germany.

The Middle East & Africa are estimated to be significantly growing with share of 3% in the medical devices market, due to the increasing adoption of advanced technologies and growing research activities. The increasing funding by the government and private organizations, and collaborations among key players, enable the development of innovative medical devices. The rising healthcare expenditure and favorable regulatory support also contribute to market growth. The rising prevalence of chronic disorders encourages patients to use medical devices for effective and targeted treatment.

UAE Market Trends

In the UAE, every 1 in 3 people suffers from one or more chronic conditions. The Ministry of Health and Prevention (MOHAP) is responsible for the regulation and approval of medical devices in the UAE. The MOHAP announced the UAE Federal Budget 2025 of AED 71.5 billion for the healthcare sector.

South Africa Market Trends

The International Diabetes Federation (IDF) demonstrated that there were over 38 million diabetes cases in South Africa in 2024. South Africa depends on imports of medical devices mainly from the U.S. and EU nations. The International Trade Administration (ITA) projected $132.68 million of medical device exports from South Africa in 2024.

Latin America is expected to grow at a notable CAGR of 6.52% in the foreseeable future. The market is primarily driven by the increasing prevalence of chronic disorders, the rising adoption of advanced technologies, and favorable regulatory support. Latin American countries focus on the indigenous development of medical devices, reducing reliance on imports from other nations. Government bodies launch initiatives to boost the medical device sector and also provide funding.

Brazil Market Trends

The medical devices market in Brazil is mainly supported by imports from other nations, particularly the U.S. The Brazilian government announced an investment of around $480 million for the purchase of more than 10,000 medical devices to be used in basic care and surgical procedures. However, efforts are made to support the indigenous development of medical devices.

Varun Suri, CEO of Dr Morepan, commented on the launch of a weight management product, LightLife, that the company aims to establish itself in the wellness market. He added that the company also aims to build long-term brands in India’s wellness market, targeting Rs 200 crore in revenue from the LightLife brand by 2030.

By Type

By End-User

By Region

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar