March 2026

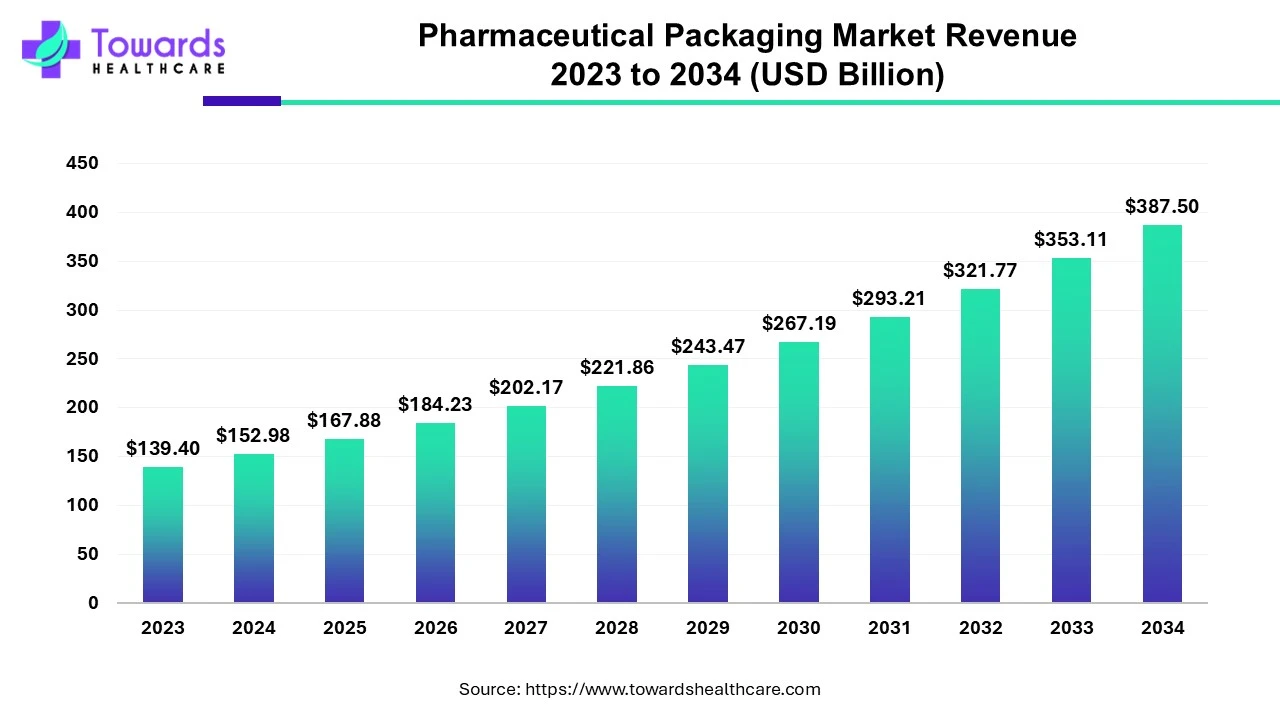

The global pharmaceutical packaging market was estimated at US$ 184.23 billion in 2026 and is projected to grow to US$ 425.25 billion by 2035, rising at a compound annual growth rate (CAGR) of 9.74% from 2026 to 2035.

| Key Elements | Scope |

| Market Size in 2025 | USD 167.88 Billion |

| Projected Market Size in 2035 | USD 425.25 Billion |

| CAGR (2025 - 2035) | 9.74% |

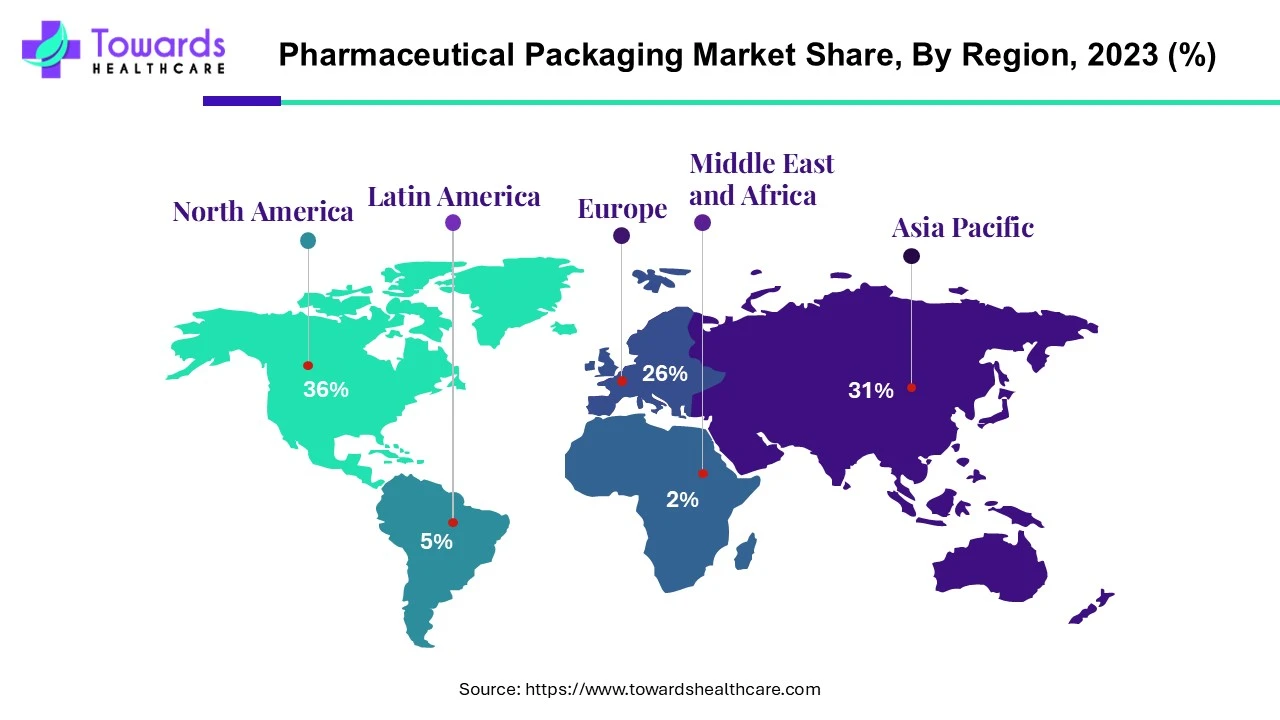

| Leading Region | North America by 36% |

| Market Segmentation | By Material, By Product, By Drug Delivery Mode, By End-use, By Region |

| Top Key Players | Amcor plc, Comar, LLC, WestRock Company, Berry Global, Inc., Owens Illinois, Inc., Schott AG, SGD Pharma, West Pharmaceutical Services, Inc., Gerresheimer AG, Vetter Pharma International, CCL Industries, Inc., Drug Plastics Group, Becton, Dickinson, and Company, AptarGroup, Inc., International Paper, PCI Pharma Services |

Packaging is the technology, art, and science of enclosing and protecting products for storage, distribution, sale, and use. The market deals with the evaluation, design, and production of pharmaceutical packaging. Pharmaceutical packaging provides identity, protection, convenience, information, stability, and integrity to the products. Apart from this, packaging is also important for promoting the products. There has been a growing demand for pharmaceutical products, which has increased the packaging process. Different packaging materials are used at the primary and secondary levels, depending on the type of the products. Pharmaceutical packaging has strict regulatory compliance compared to regular products as it is associated with health and safety. Companies need to ensure that packaging is done properly to avoid any damage or counterfeiting.

AI can be used in different stages of the pharmaceutical industry's packaging process. AI can be used to design and manufacture packages. Machine learning has been implemented to identify gaps and errors in equipment and processes, which is useful in reducing risks that can arise in assembly lines. Machine vision is used during packaging to identify defects in packages as well as products. The inspection systems are also being automated using AI to reduce human error, identify risk at an early stage, and minimize losses. Apart from the production line, AI is also being used to develop smart packaging, which consists of sensor technology capable of providing information related to viability, freshness, and other aspects of the products.

For instance,

Branded drugs are high in cost and are not affordable for everyone. Therefore, generic drugs are gaining popularity due to their lower cost and the same effect as branded drugs. Many companies invest in the production of generic drugs, and these drugs are produced in large amounts. These generic drugs needed to be packaged properly for storage, distribution, and sales. As the demand for generic drugs grows in the future, the packaging of generic products will also grow.

For instance,

The pharmaceutical packaging industry is strictly regulated by National and International Governments and agencies. Patient safety is of utmost priority, due to which not only the pharmaceutical products but also the final packaged products go through strict regulations. It becomes challenging for organizations to develop unique and high-quality packaging. Counterfeiting is one of the common issues that is faced by the companies due to which companies develop packaging that can help the consumers differentiate between real and fake products.

Smart Packaging is a Growth Opportunity for the Market

The organization is using advanced technology to develop smart packaging. The pharmaceutical packaging market is anticipated to grow due to the development of more smart packaging solutions in the future. The major focus of smart packaging is to prevent counterfeiting. These smart packaging include holograms, NFC, RFID, and QR codes that cannot be copied to produce fake products. Apart from this, smart packaging can also be used to monitor self-life, process information, track products, and administer simple packaging. With technological advancements, IoT is also being integrated into smart packaging for exchanging data.

Which Material Segment Dominated the Pharmaceutical Packaging Market?

By material, the plastics & polymers segment held the dominant share of the market. Pharmaceutical packaging materials are essential for maintaining the safety, effectiveness, and stability of drugs and pharmaceutical goods by protecting them from contamination and damage. Tamper-evident protection is achieved by the use of appropriate package materials, which helps deter the use of counterfeit medications. Because it is lightweight, affordable, and simple to manufacture, plastic packaging is frequently utilized in products, including bottles, blister packs, and prefilled syringes. Polyvinyl chloride (PVC), polyethylene terephthalate (PET), polyethylene (PE), and polypropylene (PP) are common polymers used in primary packaging.

The Paper & Paperboard Segment is Growing Significantly

By material, the paper & paperboard segment is estimated to grow significantly in the pharmaceutical packaging market during the predicted period. For solid dosage forms, such as tablets and capsules, paper-based materials are frequently utilized, including sachets, cartons, and blister pack backing. To improve their barrier qualities and guarantee that the drug is adequately protected, they might be laminated or coated with additional materials. Paper and paperboard are used in primary, secondary, and tertiary packaging. This material is mainly used in secondary packaging to give identity and information about the products and in tertiary packaging to provide additional protection, storage, and distribution.

For instance,

Why Did the Primary Segment Dominate the Pharmaceutical Packaging Market?

By product, the primary segment dominated the market and is expected to grow at the fastest rate during the forecast period. Primary packaging is the main packaging that comes in contact with the pharmaceutical products. The material used in primary packaging provides protection and stability and maintains the quality and sterility of the products from the point of manufacturing till the expiry date. Different materials such as plastic, glass, aluminum, and paper are used for making vials, tablets, prefilled syringes, bottles, caps, and so on. Depending on the type of product, a single or combination of different materials is used to ensure the safety and quality of the products.

How the Oral Drugs Segment Dominated the Pharmaceutical Packaging Market?

By drug delivery mode, the oral drugs segment dominated the market. Oral drugs are produced in the largest amounts and hence promote the growth of the pharmaceutical packaging industry. Oral drugs come in various forms, such as capsules, solid tablets, powders, and chewable tablets. Apart from this, various pharmaceuticals, such as cough syrups and oral vaccines, come under the category of oral products that are packaged on a large scale. With the rise in generic medicines and over-the-counter products, the demand for oral drugs has increased.

For instance,

The Injectables Segment is the Fastest Growing

By drug delivery mode, the injectables segment is anticipated to grow at the fastest CAGR in the pharmaceutical packaging market during 2024-2034. When choosing the appropriate injectable medication delivery system and packaging materials, there are a number of things to take into account. These include the drug's properties, such as shelf life and stability in relation to temperature, light, moisture, and oxygen, as well as how and where it will be delivered. When used in drug-device combination products, primary packaging materials must provide continued stability, sterility, purity, and the qualities necessary to ensure the intended device performance. The typical glass used for pharmaceutical main packaging is called borosilicate type I glass. Additionally, plastics offer flexibility that might be useful in various sterile injectable medication delivery-related applications.

What Made Pharma Manufacturing the Dominant Segment in the Pharmaceutical Packaging Market?

By end-use, the pharma manufacturing segment held the largest share of the market and is expected to grow at the fastest rate during the predicted period. Pharma companies have their own packaging plants, especially for primary packaging. The companies also have their own patented designs to avoid counterfeiting. Lastly, these companies have their own warehouses in which pharmaceutical products are stored and taken for distribution after tertiary packaging. There has been significant growth in the pharmaceutical industry due to the growing demand for medicines. Investments by the Government and collaboration among market players have created new opportunities for the market’s growth.

")

By region, North America dominated the pharmaceutical packaging market share by 36% in 2023. North America has the largest pharmaceutical industry. Apart from this, continuous research & development, and investment are taking place for the development of new products. There is an increasing demand for pharmaceutical products in North America due to the growing cases of cancer, diabetes, obesity, other chronic conditions, and infectious diseases. Two major countries that contribute to the market’s growth are the U.S. and Canada.

The U.S. holds the largest share of the pharmaceutical packaging market in North America due to the presence of the largest pharmaceutical sector. The Center for Drug Evaluation and Research (CDER) has more than 4,800 manufacturing sites, out of which 40% of sites are in the U.S. CDER has 140,000 application and non-application products in their catalog.

Canada is also a significant contributor to the market's growth. The exports and imports of pharmaceutical products in Canada are significant. According to the Government of Canada, there was an increase in exports and imports from 38% to 55% from 2018-2022, respectively. In 2022, Canada had a domestic pharmaceutical export of US$ 12.79 billion and an import of US$ 30.21 billion.

By region, Asia Pacific is expected to grow at the fastest rate during the forecast period. The pharmaceutical packaging market is growing strongly in Asia Pacific due to the growing investment in the pharmaceutical industry. Governments and different pharmaceutical players are investing in Asia Pacific due to the region's strong growth potential. The region has the largest population, and the population is growing with a significant increase in the number of patients. The large patient pool has increased the demand for pharmaceutical products in Asia Pacific, which has also increased the demand for pharmaceutical packaging. Several countries majorly contribute in the market’s growth. These countries are China, India, Japan, and South Korea.

China dominates the pharmaceutical packaging market in Asia Pacific. The country is known for its technological advancements, strong pharma industry, and innovation. Apart from this, the country also has a large population, which promotes market growth. China is the largest producer of active pharmaceutical ingredients (APIs) on a global level, and overall, it has the second-largest pharmaceutical industry in the world. The government of China also launched the ‘Made in China 2025’ initiative, under which various goals were established. One of the goals was to make China self-dependent in producing pharmaceutical products.

For instance,

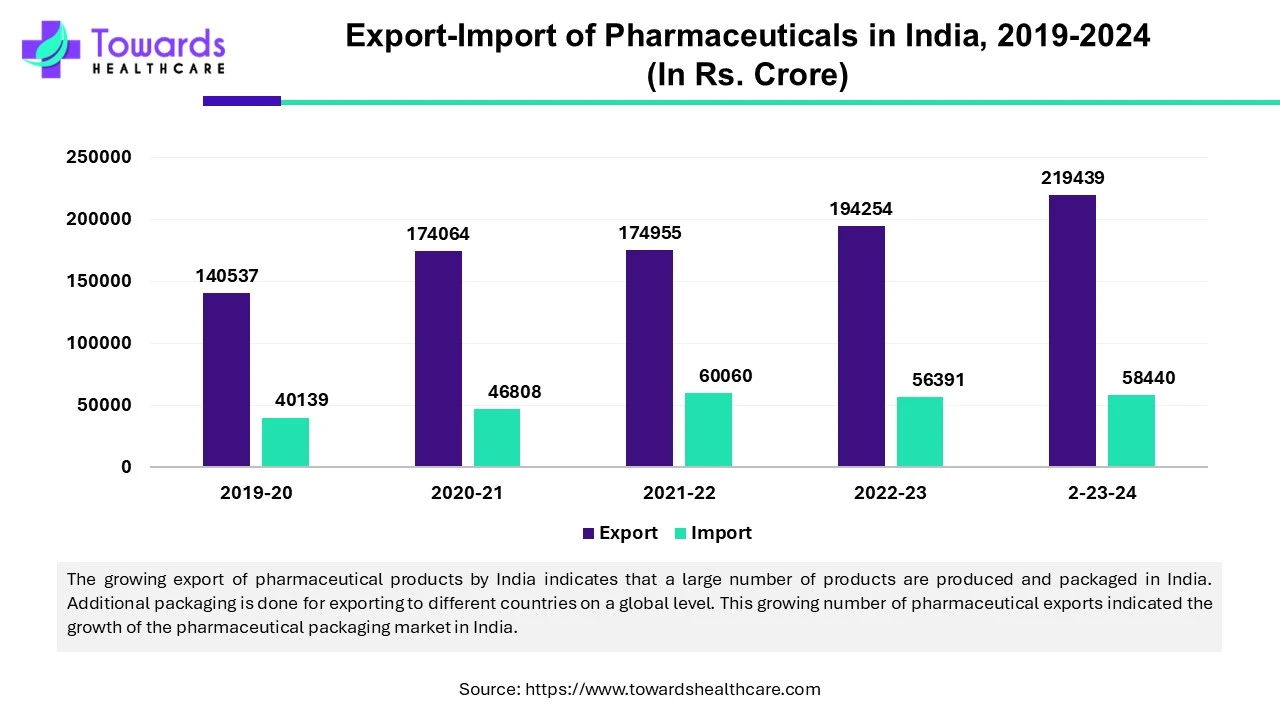

India is also a significant contributor to the pharmaceutical packaging market as the country has the 3rd largest pharmaceutical industry. India is the largest supplier of generic medicines, with a global share of 20%. The country manufactures 60,000 different generic brands in 60 categories of therapeutics. According to the Department of Pharmaceuticals, the annual turnover of India’s pharmaceutical industry in 2023-2024 was Rs. 4,17,345 Crores.

")

Europe is expected to grow significantly in the pharmaceutical packaging market during the forecast period. Europe is experiencing a rise in the demand for the use of biologics, biosimilars, gene therapies, etc. Thus, to keep these treatment options stable for a long duration or during their transportation, the use of proper packing is increasing. At the same time, biodegradable packaging is also being developed to minimize the waste produced by it and make it eco-friendly. Furthermore, the government is also supporting these developments by providing investments, as well as the regulatory bodies are also encouraging these practices.

Due to the increasing demand for the use of biologics or biosimilars, the requirement for the use of vials that can protect these formulations from degradation is rising. At the same time, this is also increasing their transportation. Thus, to protect these as well as other products, eco-friendly secondary as well as tertiary packaging is also being developed. This is supported by the government incentives provided.

The industries in Germany are focused on the development of strong and thermo-protective primary packaging to protect the thermosensitive products. Similarly, environment-friendly packaging is also being developed. This further leads to increasing collaborations to enhance the manufacturing process.

Latin America is expected to grow at a considerable CAGR in the upcoming period. The burgeoning pharmaceutical sector and favorable government support drive the market. The region is focusing on establishing manufacturing and supply chain infrastructure for pharmaceuticals. Government organizations provide funding to support the manufacturing and trade of pharmaceuticals within the region and internationally. Moreover, the rising adoption of advanced technologies also contributes to market growth. Developers focus on making smart packaging for pharmaceuticals.

Costa Rica Market Trends

In August 2025, SteinCares announced the opening of its secondary packaging facility for the packaging and distribution in Costa Rica. Costa Rica is a key logistics hub for regional distribution. The new facility will enable SteinCares to centralize supply chain management and respond more efficiently to each country’s specific needs.

| Company Name | PCI Pharma Services |

| Headquarters | Pennsylvania, U.S., North America |

| Recent Development |

In September 2024, in order to assist assembly and packaging activities, PCI Pharma Services said that it is investing over $365 million in infrastructure. With a focus on injectable forms, the investment supports the final assembly and packaging of medication-device combination products at the clinical and commercial scales using cutting-edge drug delivery methods. |

| Company Name | SGD Pharma |

| Headquarters | France, Europe |

| Contributions | SGD Pharma is a global leader in glass pharmaceutical packaging. The company is responsible for the production of more than 8 million bottles and vials in its manufacturing plants in Europe and Asia. In 2023, the company’s turnover was 441 M€. The company has 5 manufacturing plants, 7 furnaces, 1 sorting facility, and 1 decoration workshop. SGD Pharma is a global leader in glass pharmaceutical packaging. The company is responsible for the production of more than 8 million bottles and vials in its manufacturing plants in Europe and Asia. In 2023, the company’s turnover was 441 M€. The company has 5 manufacturing plants, 7 furnaces, 1 sorting facility, and 1 decoration workshop. |

By Material

By Product

By Drug Delivery Mode

By End-use

By Region

March 2026

February 2026

February 2026

February 2026