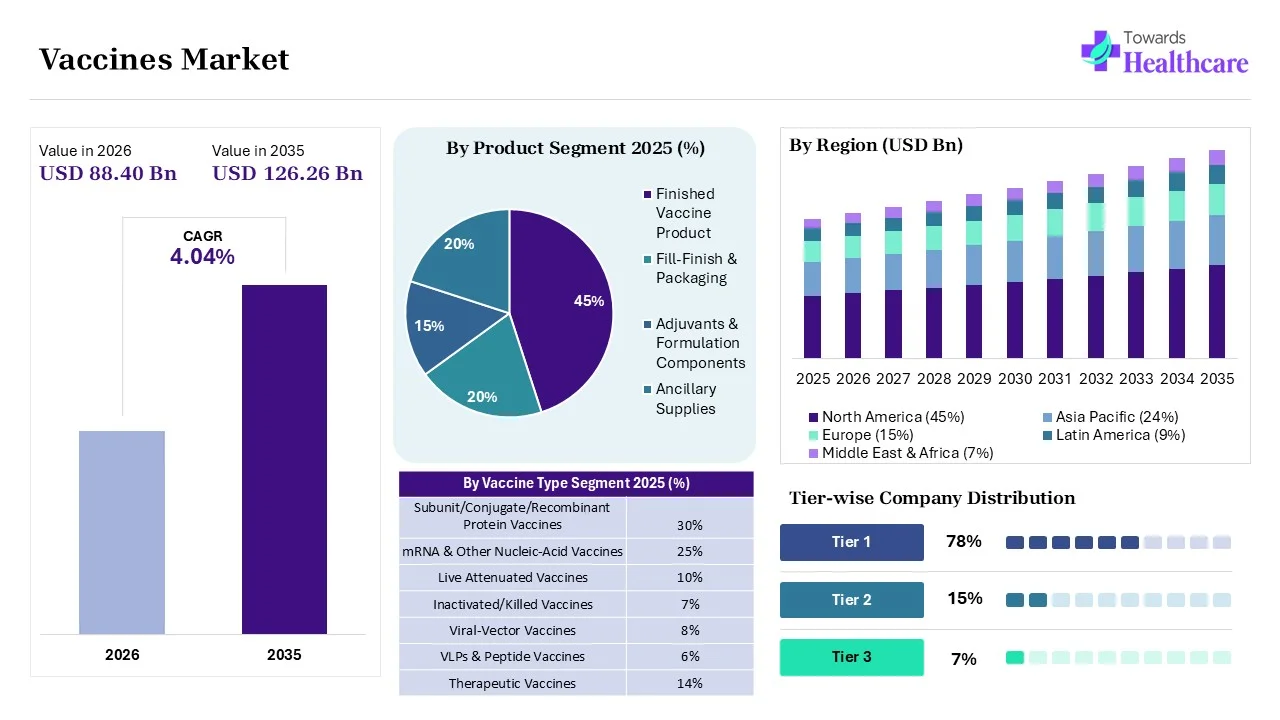

The global vaccines market size is calculated at USD 84.97 billion in 2025, grew to USD 88.40 billion in 2026, and is projected to reach around USD 126.26 billion by 2035. The market is expanding at a CAGR of 4.04% between 2025 and 2035.

")

The vaccines market is primarily driven by the growing need for vaccinations and the increasing prevalence of infectious disorders. This is supported by government initiatives that create awareness among the general public. The rising investments, public-private partnerships, and mergers & acquisitions promote market growth. Artificial intelligence (AI) facilitates the development of novel vaccines with reduced adverse effects. The future looks promising, with advancements in genomic technologies.

The vaccines market covers research, development, manufacturing, distribution, and administration of prophylactic and therapeutic vaccines for humans (and, where relevant, animal/veterinary crossover). It includes traditional platforms (live attenuated, inactivated), subunit/conjugate/recombinant vaccines, viral-vector vaccines, mRNA and other nucleic-acid platforms, protein-based vaccines, adjuvants, and delivery/administration systems. The market spans public immunization programs, private vaccination, travel medicine, outbreak response, and growing therapeutic vaccines (e.g., oncology).

Vaccination Drive: In August 2025, the Tirunelveli district of Tamil Nadu in India organized a vaccination drive against Japanese Encephalitis, a vector-borne disease spreading through Culex vishnui mosquitoes. The drive included special camps in the schools and the anganwadis to protect children.

New Product Launch: In March 2025, the Vaccine Alliance (Gavi), UNICEF, WHO, and Dalberg, Burundi, announced the launch of the malaria vaccine into its routine immunization programme. The event follows the arrival of 544,000 doses of malaria vaccines in Burundi in January 2025 and the approval of the RTS.S malaria vaccine by ABREMA.

AI can revolutionize the development of vaccines, offering unprecedented opportunities to expedite the process. It leverages genomic data, protein structures, and immune system interactions to predict antigenic epitopes and assess immunogenicity. AI and machine learning (ML) algorithms can analyze vast amounts of data and assist researchers in identifying vaccine targets. Moreover, AI and ML can be used to improve delivery efficiency and vaccine stability by developing novel drug delivery systems. They can also predict outcomes through real-time monitoring of patients.

Driver

Immunization Programs

The major growth factor for the vaccines market is the implementation of immunization programs by government and private agencies. The World Health Organization (WHO) launches immunization programs and collaborates with governments of various countries to promote vaccination. The “Essential Programme on Immunization” aims to strengthen vaccine programs, supply, and delivery, ensuring universal access to all relevant vaccines. These practices raise awareness among the general public about the importance of timely vaccination.

Restraint

Adverse Reactions

Vaccines have certain adverse effects, such as redness or soreness at the injection site, fever, and allergic reactions. Some vaccines also cause serious side effects, such as seizures or life-threatening reactions. This creates discomfort for patients, limiting their use.

Opportunity

What is the Future of the Vaccines Market?

The market future is promising, driven by advancements in genomic technologies. The latest advancements enable researchers to develop innovative vaccines, such as mRNA and DNA vaccines. These molecules are delivered through plasmid vectors or through a co-formulation of the RNA encapsulated in lipid nanoparticles. Additionally, metagenomic analysis enables researchers to determine characteristics of microbial genomes and biology, such as metabolic capacities, signs of host co-evolution, and community-wide selection. Advances in genomic technologies also facilitate rapid target identification of novel vaccine antigens.

| Table | Scope |

| Market Size in 2026 | USD 88.4 Billion |

| Projected Market Size in 2035 | USD 126.26 Billion |

| CAGR (2026 - 2035) | 4.04% |

| Leading Region | North America by 45% |

| Key Applications | Infectious disease prevention (COVID-19, influenza, HPV), travel vaccines, pediatric immunization, oncology vaccines, pandemic preparedness |

| Primary End Users | Governments, public health agencies, hospitals, clinics, NGOs (WHO, UNICEF procurement programs), retail pharmacies |

| Key Growth Drivers | Rising immunization programs, pandemic preparedness, mRNA technology adoption, increasing infectious disease burden, government funding |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | Pfizer / BioNTech, Moderna, Johnson & Johnson (Janssen), GlaxoSmithKline (GSK), Sanofi Pasteur, Merck & Co. (MSD), AstraZeneca, Novavax, Sinovac Biotech, Sinopharm (CNBG), Serum Institute of India (SII), CSL Seqirus, Bharat Biotech, Takeda Vaccines, Valneva, Bavarian Nordic, Emergent BioSolutions, CureVac / CureVac-type developers, Bavarian Nordic |

| Top Key Players | By Vaccine Type, By Indication/Target Disease, By Product, By Distribution/Commercial Model, By Manufacturing Stage, By Region |

")

| Segments | Shares % |

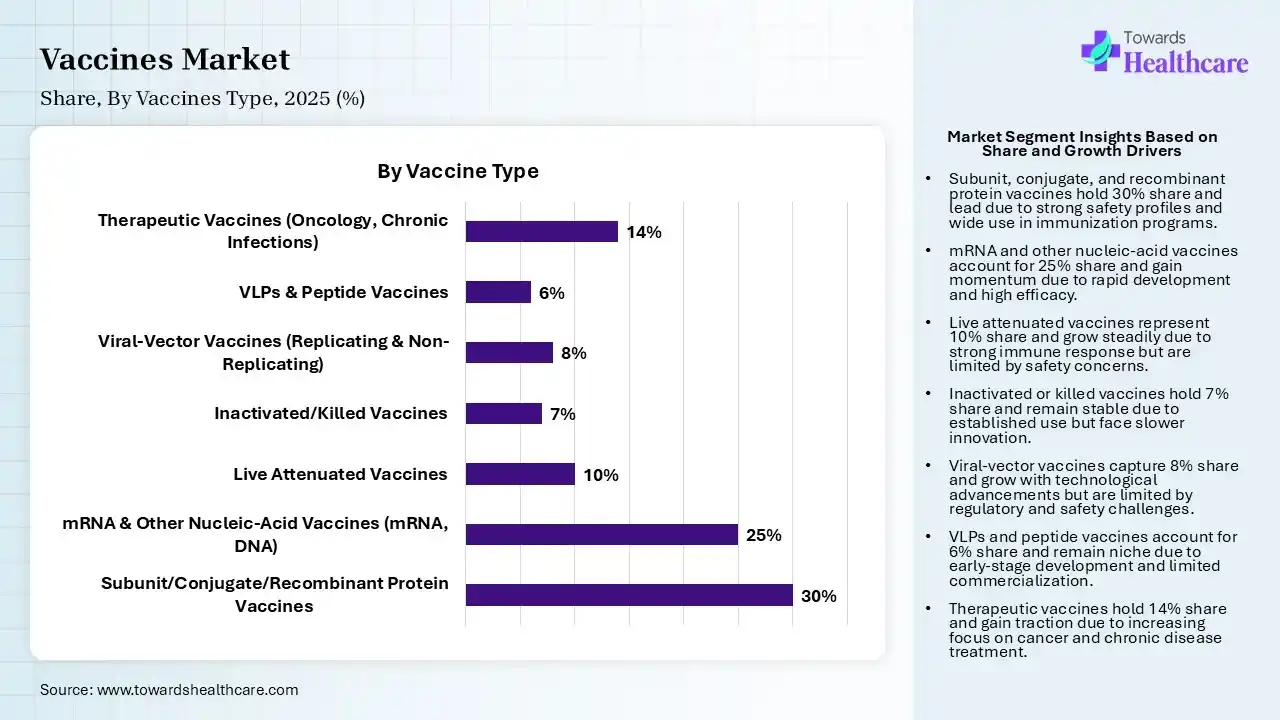

| Subunit/Conjugate/Recombinant Protein Vaccines | 30% |

| mRNA & Other Nucleic-Acid Vaccines (mRNA, DNA) | 25% |

| Live Attenuated Vaccines | 10% |

| Inactivated/Killed Vaccines | 7% |

| Viral-Vector Vaccines (Replicating & Non-Replicating) | 8% |

| VLPs & Peptide Vaccines | 6% |

| Therapeutic Vaccines (Oncology, Chronic Infections) | 14% |

Explanation

Which Vaccine Type Segment Dominated the Vaccines Market?

By vaccine type, the subunit/conjugate/recombinant protein vaccines segment held a dominant presence in the market by 30% share in 2025. This is due to advancements in recombinant technology and the ability to prevent a wide range of diseases. They can prevent many infectious diseases, such as RSV, HIV, COVID-19, Ebola, and influenza. Recombinant protein vaccines account for over 30% of vaccine candidates, most of which focus on spike proteins of the virus. They offer numerous benefits, including safety, effectiveness, and ease of manufacturing.

By vaccine type, the mRNA and other nucleic-acid vaccines segment is expected to grow at the fastest CAGR in the market during the forecast period. Nucleic acid vaccines introduce a piece of genetic material that corresponds to a viral protein. They do not contain live virus, making them suitable and safer for a wide patient population. They are easily adaptable to different strains and pathogens, targeting multiple pathogens in a single vaccine. Additionally, mRNA vaccines can be produced on a large scale rapidly and efficiently.

")

| Segments | Shares % |

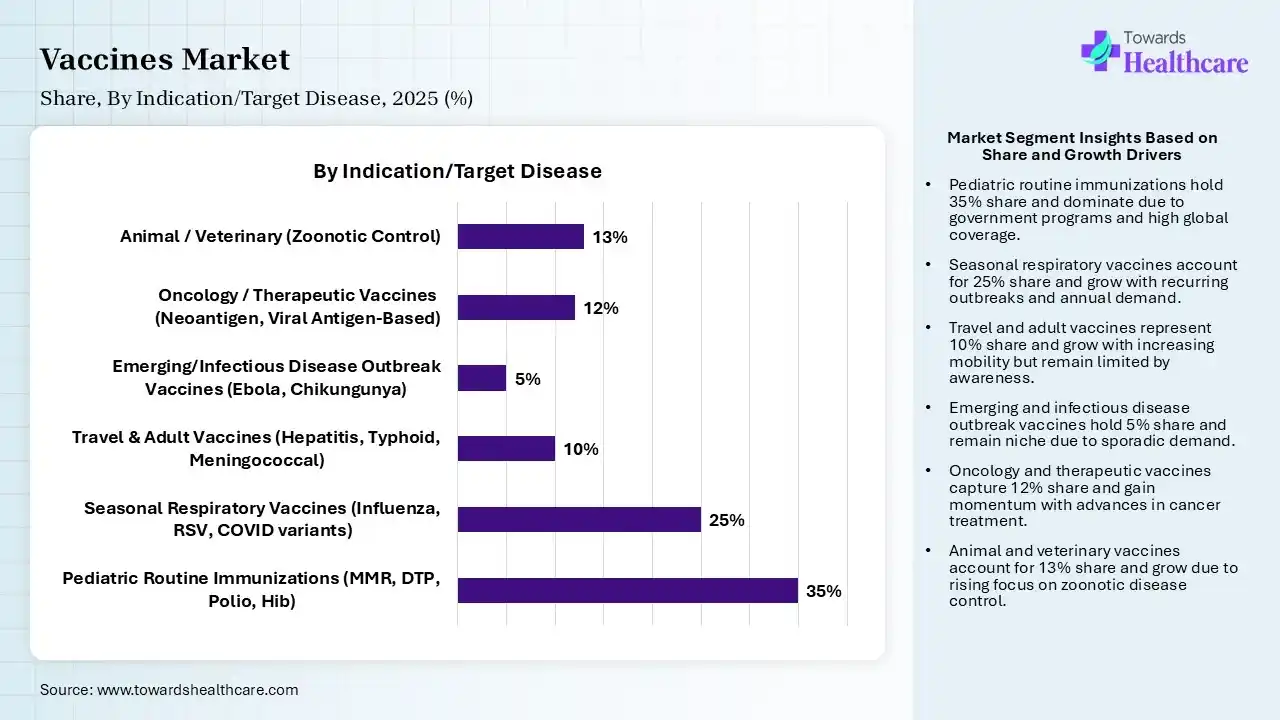

| Pediatric Routine Immunizations (MMR, DTP, Polio, Hib) | 35% |

| Seasonal Respiratory Vaccines (Influenza, RSV, COVID variants) | 25% |

| Travel & Adult Vaccines (Hepatitis, Typhoid, Meningococcal) | 10% |

| Emerging/Infectious Disease Outbreak Vaccines (Ebola, Chikungunya) | 5% |

| Oncology / Therapeutic Vaccines (Neoantigen, Viral Antigen-Based) | 12% |

| Animal / Veterinary (Zoonotic Control) | 13% |

Explanation

How the Pediatric Routine Immunizations Segment Dominated the Vaccines Market?

By indication/target disease, the pediatric routine immunizations segment held the largest revenue share of the market by 35% share in 2025. The increasing number of babies born and growing awareness of routine immunizations boost the segment’s growth. Different vaccines against RSV, hepatitis B, pneumococcal, polio, influenza, chickenpox, and hepatitis A diseases are administered to children from birth to adolescence. Childhood vaccination can reduce the burden of disease morbidity and mortality cost-effectively. The WHO reported that approximately 3.5 to 5 million deaths are prevented annually through immunization.

By indication/target disease, the seasonal respiratory vaccines segment is expected to grow with the highest CAGR in the market during the studied years. The rising prevalence of infectious respiratory disorders and the growing need for preventing epidemics augment the segment’s growth. There are around a billion cases of seasonal influenza annually, including 3-5 million cases of severe illness. Immunizations are a core prevention strategy to reduce the risk of respiratory viruses.

")

| Segments | Shares % |

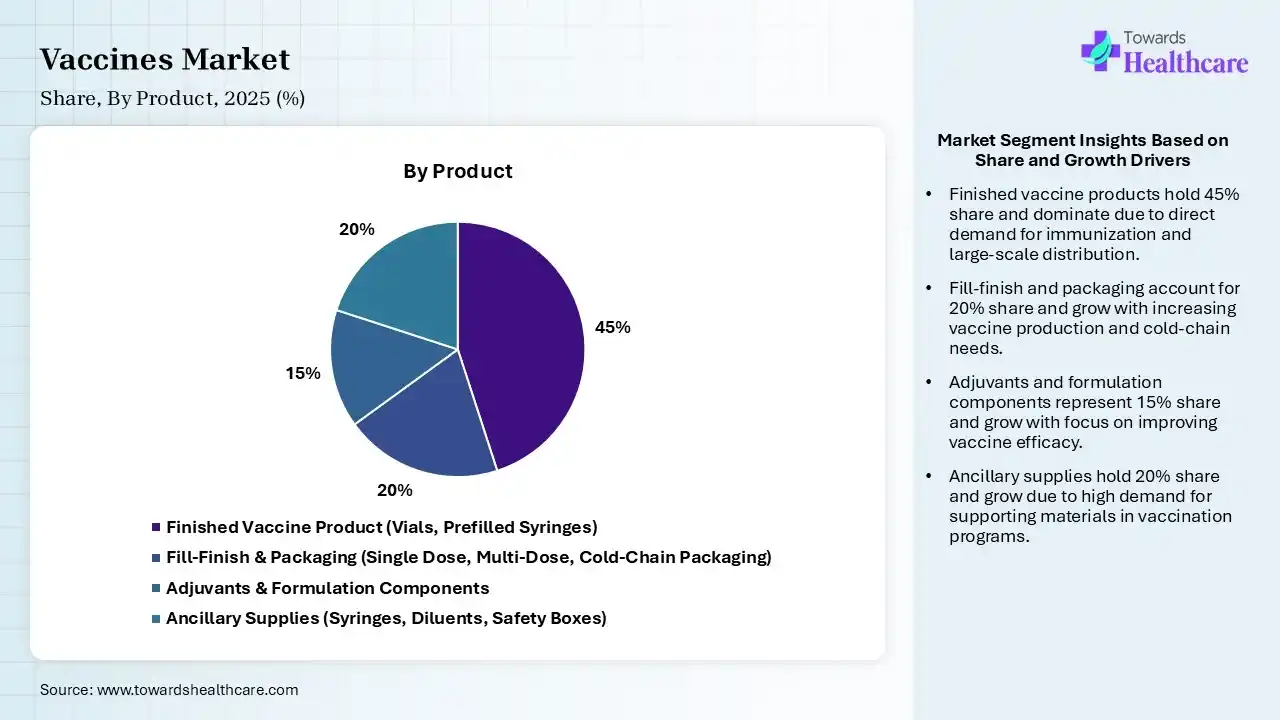

| Finished Vaccine Product (Vials, Prefilled Syringes) | 45% |

| Fill-Finish & Packaging (Single Dose, Multi-Dose, Cold-Chain Packaging) | 20% |

| Adjuvants & Formulation Components | 15% |

| Ancillary Supplies (Syringes, Diluents, Safety Boxes) | 20% |

Explanation

Why Did the Finished Vaccine Product Segment Dominate the Vaccines Market?

By product, the finished vaccine product segment contributed the biggest revenue share of the market by 45% in 2025. This is due to the ease of administration and widespread availability. Finished vaccine products are more stable as they undergo the complete production process. They eliminate the need for sample preparation before administration, saving the time of healthcare professionals. The availability of pre-filled syringes also simplifies vaccine administration, reduces dosing errors and wasted product, and minimizes the risk of cross-contamination.

")

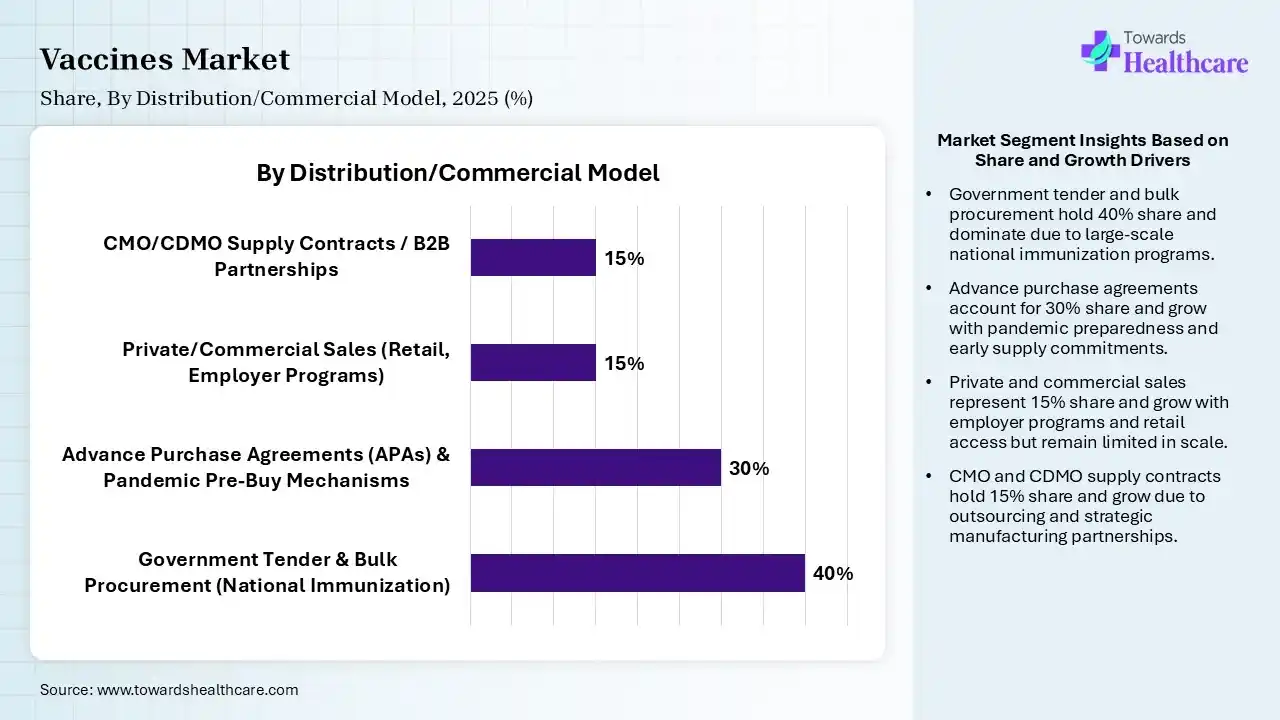

| Segments | Shares % |

| Government Tender & Bulk Procurement (National Immunization) | 40% |

| Advance Purchase Agreements (APAs) & Pandemic Pre-Buy Mechanisms | 30% |

| Private/Commercial Sales (Retail, Employer Programs) | 15% |

| CMO/CDMO Supply Contracts / B2B Partnerships | 15% |

Explanation

Which Distribution/Commercial Model Segment Led the Vaccines Market?

By distribution/commercial model, the government tender & bulk procurement segment led the global market by 40% share in 2025. The segmental growth is attributed to the increasing national immunization programs and the need to potentiate accessibility to cater to a large patient population. Government organizations procure vaccines to distribute at affordable rates, especially to people from low- and middle-income countries. This increases access to people, even from rural areas.

By distribution/commercial model, the advance purchase agreements (APAs) & pandemic pre-buy mechanisms segment is expected to witness the fastest growth in the market over the forecast period. APAs are a part of a strategy to provide upfront financing for vaccines and to accelerate their development and availability. They expedite the R&D process and de-risk company investments. The demand for APAs increased during the COVID-19 pandemic to potentiate the development of vaccines.

")

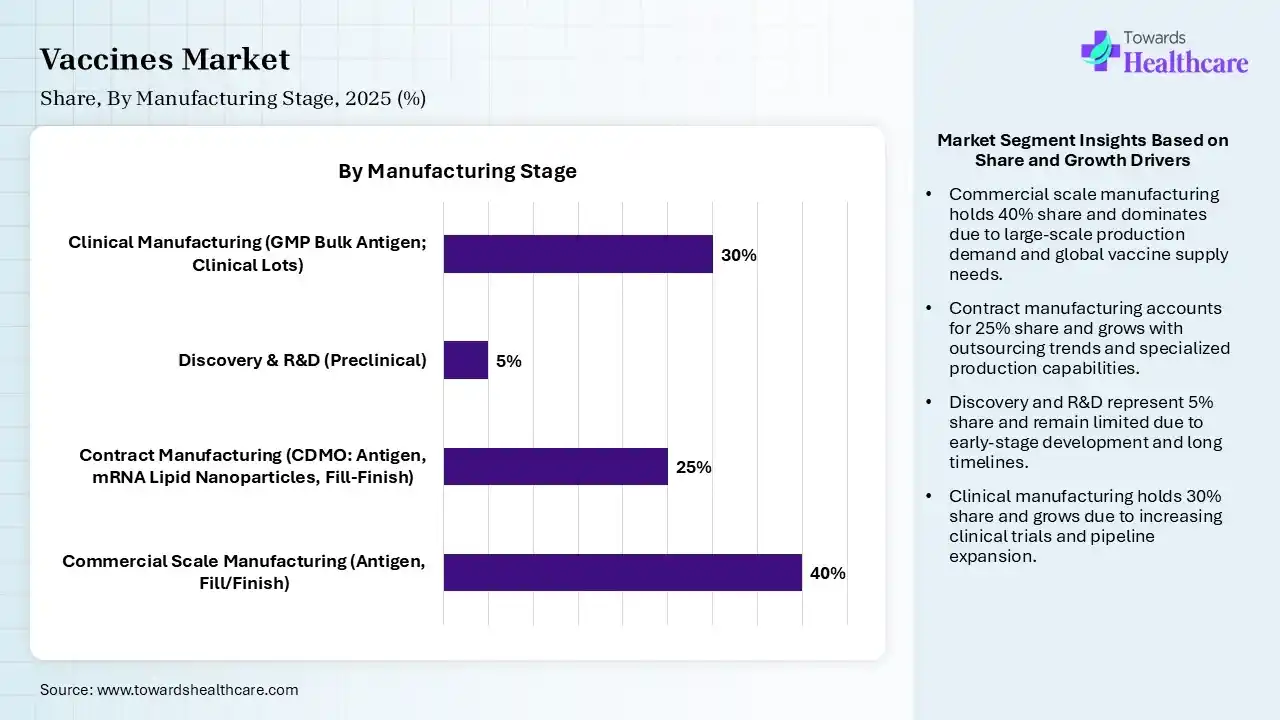

| Segments | Shares % |

| Commercial Scale Manufacturing (Antigen, Fill/Finish) | 40% |

| Contract Manufacturing (CDMO: Antigen, mRNA Lipid Nanoparticles, Fill-Finish) | 25% |

| Discovery & R&D (Preclinical) | 5% |

| Clinical Manufacturing (GMP Bulk Antigen; Clinical Lots) | 30% |

Explanation

What Made Commercial Scale Manufacturing the Dominant Segment in the Vaccines Market?

By manufacturing stage, the commercial scale manufacturing segment accounted for the highest revenue of 40% share of the market in 2025. This segment dominated because commercial-scale manufacturing fulfills the needs of a diverse patient population. Large biotechnology companies have suitable infrastructure to manufacture large quantities of vaccines. The increasing population and the growing need to prevent future pandemics potentiate the demand for commercial-scale manufacturing. The rising investments by the government and private organizations allow companies to set up their manufacturing facilities.

By manufacturing stage, the contract manufacturing segment is expected to show the fastest growth in the coming years. The increasing number of biotech startups potentiates the need for contract development and manufacturing organizations (CDMOs). CDMOs possess suitable manufacturing infrastructure and provide relevant expertise to complex research & manufacturing problems. Even large biotech companies collaborate with CDMOs to focus on core competencies, such as product sales and marketing.

")

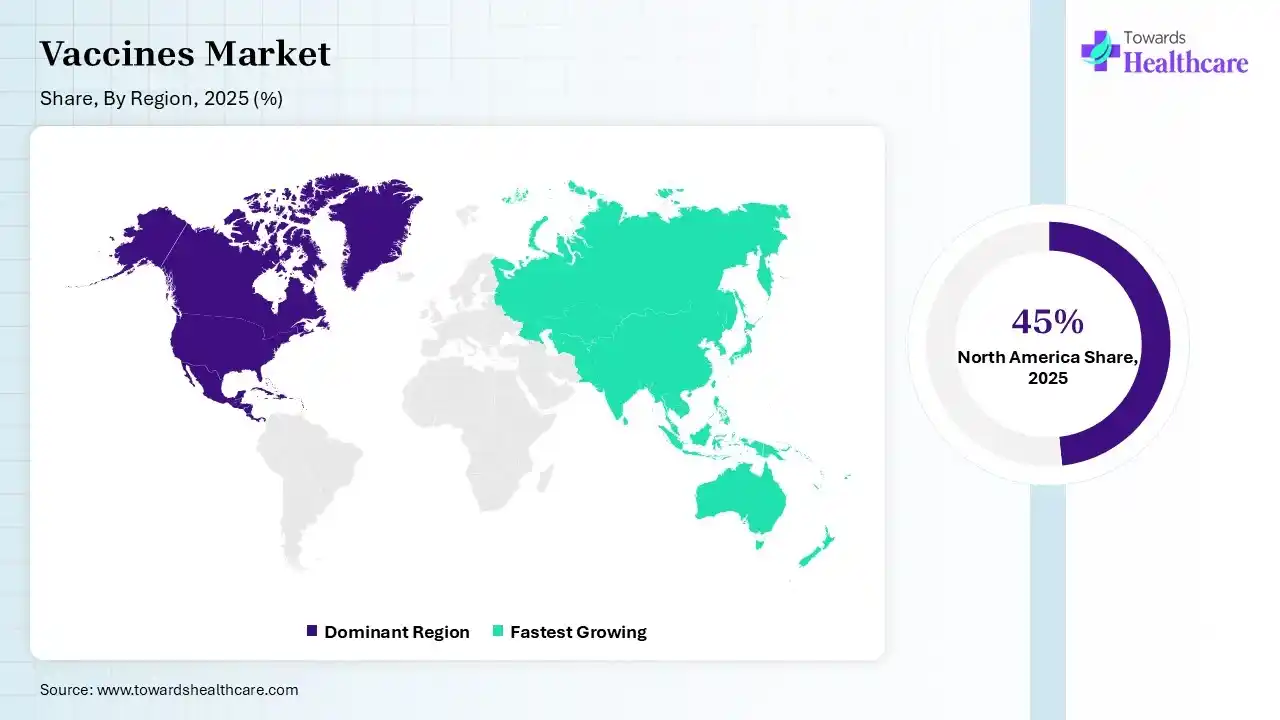

North America dominated the market by 45% share in 2025. The availability of a robust healthcare infrastructure, the presence of key players, and favorable government support are the major growth factors that govern market growth in North America. The growing research and development activities have led to the development of innovative vaccines. This results in the rising number of clinical trials.

North America Vaccine Trade Overview (HS 3002) – Import & Export Performance, 2024

| Country | Trade Flow | Trade Value (USD) | Trade Value (USD) |

|---|---|---|---|

| USA | M | $109,160,336,750 | 32,817,103 |

| X | $54,586,966,262 | 89,768,767 | |

| Canada | M | $6,625,853,265 | 0 |

| X | $1,045,524,406 | 21,821,730 | |

| Mexico | M | $2,281,628,168 | 0 |

| X | $114,466,093 | 0 |

U.S. Market Trends

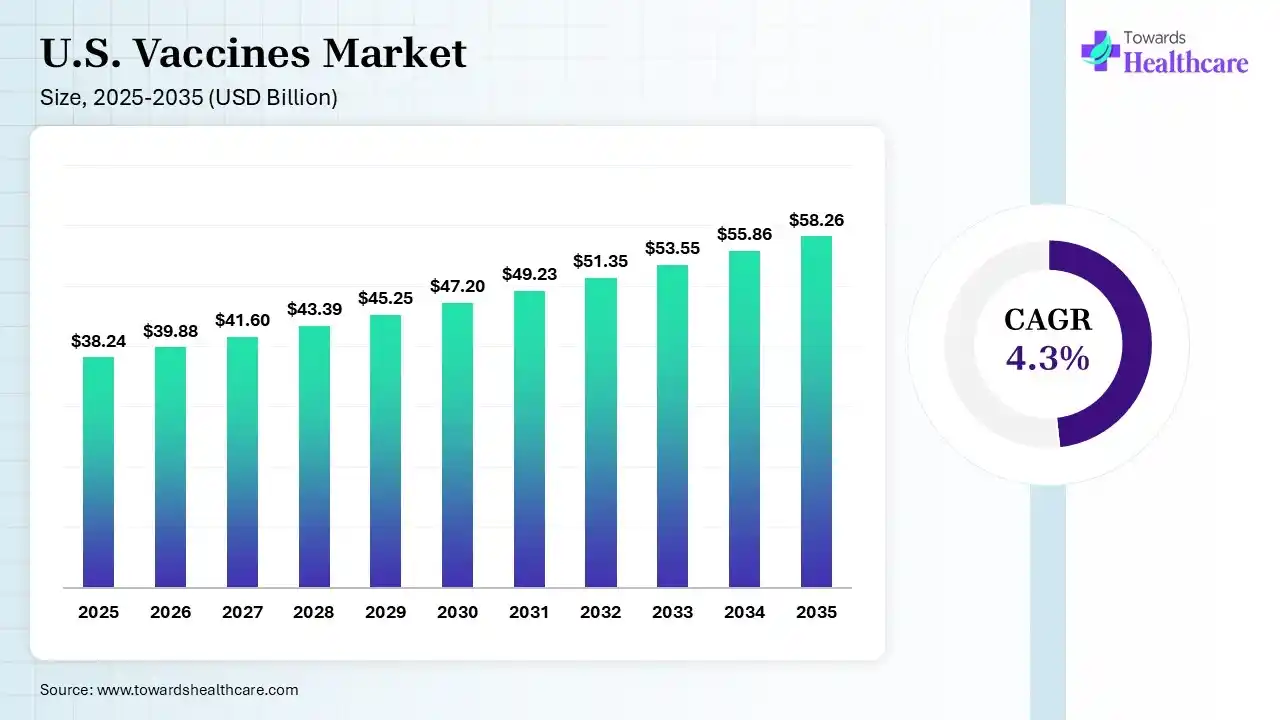

The U.S. Vaccines market size touched US$ 38.24 billion in 2025, with expectations of climbing to US$ 39.88 billion in 2026 and hitting US$ 58.26 billion by 2035, driven by a CAGR of 4.3% over the forecast period.

")

Key players, such as GlaxoSmithKline, Pfizer, and AstraZeneca, are the major suppliers of vaccines in the world. Their headquarters are situated in the U.S. The U.S. conducts the highest number of clinical trials in the world. Out of 10,771 clinical trials on the clinicaltrials.gov website, 4,207 trials are registered in the U.S. related to vaccines as of August 2025.

Canada Market Trends

The Canadian government launched a $317 million “Canada’s Global Initiative for Vaccine Equity (CanGIVE)” initiative to bolster COVID-19 vaccine delivery and increase regional vaccine manufacturing capacity during the COVID-19 pandemic era. The federal government provides childhood vaccines for free, irrespective of economic status and the province or territory.

Asia-Pacific is expected to host the fastest-growing vaccines market by 24% share in the coming years. The rising incidence of seasonal infectious diseases and increasing investments and collaborations bolster market growth. Government organizations make constant efforts to promote vaccination through immunization programs. They collaborate with private companies to deliver vaccines at affordable rates. The growing population further increases the need for vaccines. The presence of a suitable vaccine manufacturing infrastructure and affordable labor encourages foreign manufacturers in the Asia-Pacific countries.

Asia & Oceania Vaccine Trade Flow Assessment (HS 3002) – Imports, Exports & Market Share, 2024

| Country | Trade Flow | Trade Value (USD) | Net Weight (Kg) |

|---|---|---|---|

| China | M | $17,746,312,701 | 15,617,437 |

| X | $1,034,091,598 | 3,493,005 | |

| India | M | $1,191,107,001 | 3,701,282 |

| X | $1,604,900,731 | 6,382,913 | |

| Japan | M | $13,657,025,989 | 5,432,503 |

| X | $2,479,847,100 | 779,581 |

China Market Trends

The 2024-25 winter-spring influenza season in China was predominantly characterized by the circulation of influenza A (H1N1)pdm09, accounting for 97.4% of identified cases. A recent study found that the rapid decline in cases since February 2025 was attributed to delayed vaccine effects and accumulated immunity. Approximately 2.46% of the general population was covered with influenza vaccination.

India Market Trends

As of December 2024, more than 20,414 Indians were infected with swine flu (H1N1). The Indian government provides free vaccination services to 2.9 crore pregnant women and 2.6 crore infants annually as part of its Universal Immunization Programme (UIP). It launches targeted campaigns to address challenges among zero-dose children. The U-WIN platform tracks immunization status digitally.

Europe is expected to grow at a notable CAGR in the vaccines market by 15% share in the foreseeable future. The increasing awareness of vaccinations and the rising adoption of advanced technologies augment the market. Research laboratories and companies in European nations have a favorable research and manufacturing infrastructure to develop novel vaccines. The funding cut by the U.S. government opens doors for American scientists to conduct their research activities in Europe. Favorable trade policies also contribute to market growth.

Europe Vaccine Trade Analysis (HS 3002) – Regional Import & Export Contribution, 2024

| Country | Trade Flow | Trade Value (USD) | Net Weight (Kg) |

|---|---|---|---|

| Germany | M | $37,784,121,245 | 36,897,962 |

| X | $48,442,621,789 | 28,469,553 | |

| UK | M | $10,137,305,129 | 9,179,506 |

| X | $7,087,771,968 | 19,178,025 |

Belgium Market Trends

In 2023, Belgium was the largest exporter of human-use vaccines, accounting for $15.3 billion of exports. The top importers for Belgian vaccines were China and the U.S. (Source: OEC). The other top destinations include Germany, Japan, the UK, Brazil, and France. Additionally, Belgium attracted more than 2 billion euros of investments in vaccine production.

Ireland Market Trends

Ireland was the world’s second-largest exporter of human-use vaccines in 2023, exporting vaccines worth $12.3 billion. The major destinations of vaccine export were Belgium, China, Germany, Japan, and Singapore. Vaccine was the 3rd most exported product in Ireland in 2023.

South America is expected to grow significantly in the vaccines market during the forecast period, due to growing immunization programs, where rapid urbanization is also increasing the demand for vaccinations to prevent the growing infectious diseases. The growing health awareness and shift towards preventive care are also increasing their demand, promoting the market growth.

Brazil Vaccines Market Trends

The rapid urbanization in Brazil is increasing the incidence of infectious diseases, driving the demand for vaccines. Similarly, the growing government immunization programs, expanding private healthcare, and technological advancement are also increasing their use and accessibility, as well as the development of new vaccine candidates.

MEA is expected to show lucrative growth in the vaccines market by 7% share during the forecast period, due to the growing incidence of infectious diseases, where the growing government vaccination programs are also increasing the use of various vaccines. Expanding healthcare infrastructure and investments are also driving the development of new vaccines, which are enhancing the market growth.

Saudi Arabia Vaccines Market Trends

The growing public health initiatives and vaccination programs across Saudi Arabia are increasing the demand for various vaccines. The growing shift towards preventive healthcare, increasing healthcare investments, and incidences of infectious diseases are also increasing their use, as well as innovations.

| Category | Key Participants | Role in Ecosystem |

| Technology Providers | Lipid nanoparticle tech firms, biotech R&D platforms | Enable vaccine formulation (especially mRNA, viral vector systems) |

| Product Manufacturers | Large pharma & biotech vaccine producers | Develop and commercialize vaccines at scale |

| Service Providers | Contract manufacturing organizations (CMOs), logistics firms | Support production scaling and global distribution |

| Platform Providers | mRNA, viral vector, recombinant protein platforms | Core enabling technologies for modern vaccines |

| CROs/CDMOs | Catalent, Lonza, Samsung Biologics | Clinical trial execution and large-scale manufacturing |

| Software Vendors | Clinical trial analytics, pharmacovigilance platforms | Data management, safety monitoring, regulatory reporting |

| Research Institutions | NIH, academic hospitals, WHO collaborating centers | Early-stage discovery and epidemiological research |

| End-User Industries | Healthcare systems, governments, military health agencies | Vaccine procurement and administration |

1. R&D

2. Clinical Trials and Regulatory Approvals

3. Formulation and Final Dosage Preparation

4. Packaging and Serialization

5. Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 70% | 25% | 5% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Pfizer Inc. | New York, New York | USA | One of the largest global vaccine manufacturers with strong mRNA vaccine dominance | Comirnaty (COVID-19 vaccine), Prevnar (pneumococcal vaccine) |

| Sanofi | Paris | France | Major global vaccine leader with broad immunization portfolio | Fluzone (influenza), Menactra (meningococcal), dengue vaccine |

| GlaxoSmithKline | London | United Kingdom | One of the strongest global vaccine pipelines and pediatric vaccine leader | Shingrix (shingles), Infanrix, hepatitis vaccines |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| BioNTech SE | Mainz | Germany | Key mRNA technology innovator and Pfizer partner | mRNA vaccine platform, oncology vaccine pipeline |

| CSL Seqirus | Melbourne, Victoria | Australia | Global leader in influenza vaccines and pandemic preparedness | Seasonal flu vaccines, cell-based influenza vaccines |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Bharat Biotech | Hyderabad, Telangana | India | Strong regional vaccine innovator with WHO-recognized products | Covaxin, rotavirus vaccine |

| Sinovac Biotech | Beijing | China | Key player in inactivated viral vaccines, especially COVID-19 | CoronaVac (COVID-19 vaccine) |

| Novavax | Gaithersburg, Maryland | USA | Protein subunit vaccine specialist with COVID-19 vaccine approval | NVX-CoV2373 (COVID-19 vaccine) |

Dr. Michael Osterholm, Regents Professor and Director of CIDRAP, commented that the Vaccine Integrity Project aims to make vaccine recommendations and to review safety and effectiveness. It is prudent to evaluate whether independent activities may be needed to stand in its place, and non-governmental groups can provide science-based information to the American public.

By Vaccine Type

By Indication/Target Disease

By Product

By Distribution/Commercial Model

By Manufacturing Stage

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar